Networks of impunity: Corruption and European foreign policy

Summary

- European governments have failed to prevent corrupt actors from laundering hundreds of billions of dollars through the international financial system and their own economies.

- This breakdown in the rule of law empowers kleptocratic regimes across the globe, which capitalise on the political culture underpinning Europe’s approach to globalisation.

- Western governments create a negative feedback loop that hinders their foreign policy initiatives when they treat corruption in other countries as an inherent part of the local culture.

- European policymakers should aim to catch up with, and overtake, their US counterparts on anti-money laundering regulation and enforcement.

- European countries should create national institutions – and an international coalition of Western states – that are dedicated to countering kleptocrats.

Introduction

Kleptocrats regularly exploit Europe’s financial system. In the decade since the global financial crisis, dozens of money laundering schemes linked to corrupt, abusive regimes have come to light across the continent, revealing the limits to the rule of law within European economies. The networks behind these arrangements have handled hundreds of billions of dollars stolen from public institutions and private companies, often benefiting from offshore havens across the globe – and even flows of European development funding. The process has, in effect, created massive cross-border slush funds for authoritarian leaders everywhere from North Korea to Venezuela. If European countries are to check kleptocrats’ malign activities and sustain a rules-based international order, they will need to adapt their foreign policies and enforcement regimes to the reality of illicit finance in a deeply integrated world.

They have the latent ability to achieve this. For all their internal divisions, European countries collectively make up a financial power second only to the United States. As such, their failure to halt kleptocrats’ exploitation of the financial system can seem inexplicable at first. Yet it stems from more than just governments’ apparent indifference to financial crime. Kleptocrats and their networks may rely on European enablers to move money across the globe, enhance their political influence, fight their legal battles, and guard their reputations, but some of the structures and cultures that facilitate such activity sprang from well-intentioned international cooperation and compelling economic and political arguments.

Nonetheless, recent events indicate that the threat is becoming more severe. The targeted killing of journalists who investigated kleptocrat-linked financial crime in Malta and Slovakia shows how parts of Europe could lose the democratic practices required for an open public debate on corruption. The murders contributed to a multi-year decline in press freedom in Europe and revealed fundamental weaknesses in checks and balances on government power – as shown in research by Reporters Without Borders and the Council of Europe respectively. This backsliding suggests that, when European countries tolerate the presence of international corruption networks within their economies, they risk importing practices common to life under kleptocratic regimes.

So long as kleptocrats, corruption networks, and their European enablers can range through ungoverned spaces of the financial system, they will skew parts of Europe’s economies to their advantage. They will also strengthen their influence on European politics and society, causing the destructive side of globalisation to loom large in voters’ imaginations. After all, it is difficult to enforce laws on election campaign funding or investment screening when kleptocrats can easily disguise their financial activities within shell companies, offshore havens, and lightly regulated institutions. Where the rule of law is partial and selective, these dynamics threaten to degrade the social contract.

This paper analyses the relationship between kleptocrats, finance, and European foreign policy. It argues that Europe’s passivity and, at times, complicity in cross-border corruption hinder its pursuit of a foreign policy based on the rule of law. The analysis shows how European laws and institutions have created channels of financial impunity that often undermine attempts to build a rules-based international order. By allowing illicit funds to circulate into, through, and out of their territory, European governments have sometimes helped violent and destabilising regimes stay in power.

The paper begins by discussing some of the ways in which kleptocrats acquire and use illicit funds, including their co-option of Western development programmes and private investment. Using one high-profile fraud case, it shows how kleptocrats move illicit funds through Europe, sometimes with the aim of funding military operations in places such as Syria. The paper then examines how Europe became a major destination for kleptocrats’ money, focusing on its regulatory culture and its entanglement with offshore havens. The fourth section looks at the role that European countries play in international corruption and how this impedes their ability to formulate effective foreign policy. Finally, the paper lays out some of the key measures to counter illicit finance that international organisations and Western governments have introduced in the past decade, setting out new steps they should take to dismantle kleptocrats’ financial networks.

How kleptocrats generate illicit funds

Within Europe’s channels of financial impunity, it can be hard to distinguish between thieves who have become rulers and rulers who have become thieves. Given that an array of autocratic states use European financial structures to engage in money laundering and other forms of corruption, there is no one country that exemplifies all this activity. Nonetheless, events in Russia in the past few decades illustrate how a kleptocracy can develop to both harm – and be nurtured – by European countries.

The Russian Laundromat – which moved $20.8 billion in illicit funds through bank accounts in eastern Europe (and then other regions) between 2011 and 2014 – is just one of many money laundering schemes connected to powerful figures in the country. By 2016, Russians owned as much as 60 percent of their country’s GDP in offshore wealth, a share matched only by citizens of a few states in the Gulf and Latin America. Of course, not all this wealth was held in Europe. And most Russians with assets abroad have neither a relationship with the Kremlin nor any desire to subvert democracy. But the ways in which some of Russia’s super-rich acquired their money show how a kleptocracy can quickly gain momentum.

The haphazard transition to capitalism in Russia in the 1990s initially pushed the state towards failure, before it eventually reasserted control over society through a strange alloy of Western-style financialisation, post-communist elitism, and co-option of organised crime. Political scientist Mark Galeotti writes that the Kremlin pursued two distinct approaches to this recovery. The first was the limited nationalisation of the underworld, some of whose members gained formal positions of power. The second was the gangsterisation of formal sectors, a process long in train for which the government devised new rules. In this way, Galeotti argues, “somewhere around the turn of the twenty-first century, state-building thieves and criminalised statesmen met in the middle.”

In the wild nineties, the brutality of competition for control of Russian industries – including, famously, the aluminium sector – ensured that only magnates who had substantial political protection could defeat their rivals. The process supercharged Russia’s kleptocratic networks partly because a handful of actors with the requisite political connections, ruthlessness, and luck suddenly gained access to vast resources. This allowed them to found or enlarge personal empires. Within limits set by those at the top, they could now bypass, co-opt, or ally with public institutions as needed, eliminating rivals at will. And, by moving their wealth offshore, Russian kleptocrats bought a kind of insurance against shifts in the political weather at home.

However, while kleptocratic networks expanded with unusual ferocity in Russia in the 1990s, the dynamic is not unique to either the country or the era. Scholars such as Sarah Chayes, Alexander Cooley, and John Heathershaw have shown how similar developments have occurred in states across Africa, central and south Asia, and the Middle East in the last few decades. Recent acts of kleptocracy in east Asia and the Americas – such as a former Malaysian prime minister’s alleged exploitation of the 1Malaysia Development Berhad fund, and a Venezuelan minister’s alleged support for illicit drugs networks run by Hizbullah – suggest that such expansions occur in every region and continue to this day.

These processes sometimes draw on a large influx of aid or investment from European governments or firms. They can involve everything from telecoms projects in Uzbekistan to energy contracts in South Sudan. And they span huge differences in language, economics, and politics. But, for all such variations in context, a pattern emerges time and again: state-linked corruption networks capture an influx of new resources, convert these resources into offshore slush funds, and use the proceeds to pursue their core political and economic objectives at home and abroad. In this sense, kleptocrats have created a kind of global monoculture.

Yet Western policymakers have often treated kleptocracy as a localised, natural feature of the foreign political environments they seek to shape – one they can ignore where it seemingly complicates their broader goals. They have done so especially often in war-torn countries that receive huge amounts of Western development aid and investment.

Former US army general HR McMaster observed this in Afghanistan, where he led Shafafiyat, a military anticorruption task force. McMaster argues that the international community was “passive about [corruption] and largely ignorant about the scope of the problem … its impact on the mission, the Afghan state and the Afghan people”. This passivity, he believes, led to a “simplistic interpretation of corruption that is really bigotry masquerading as cultural sensitivity: this idea that Afghans are corrupt and there’s nothing we can do about it”. Indeed, Western officials’ attitudes towards corruption appear to have been far more relaxed than those of Afghans themselves. Research conducted by the Asia Foundation across all 34 of Afghanistan’s provinces in 2012 – towards the end of Hamid Karzai’s long tenure as leader of the country – revealed that 79 percent of Afghans saw corruption as a major problem for their country, while 47 percent viewed administrative corruption as the type that affected them most. The proceeds of such graft often found their way into the offshore accounts of politically connected gangsters rather than projects that benefited most citizens.

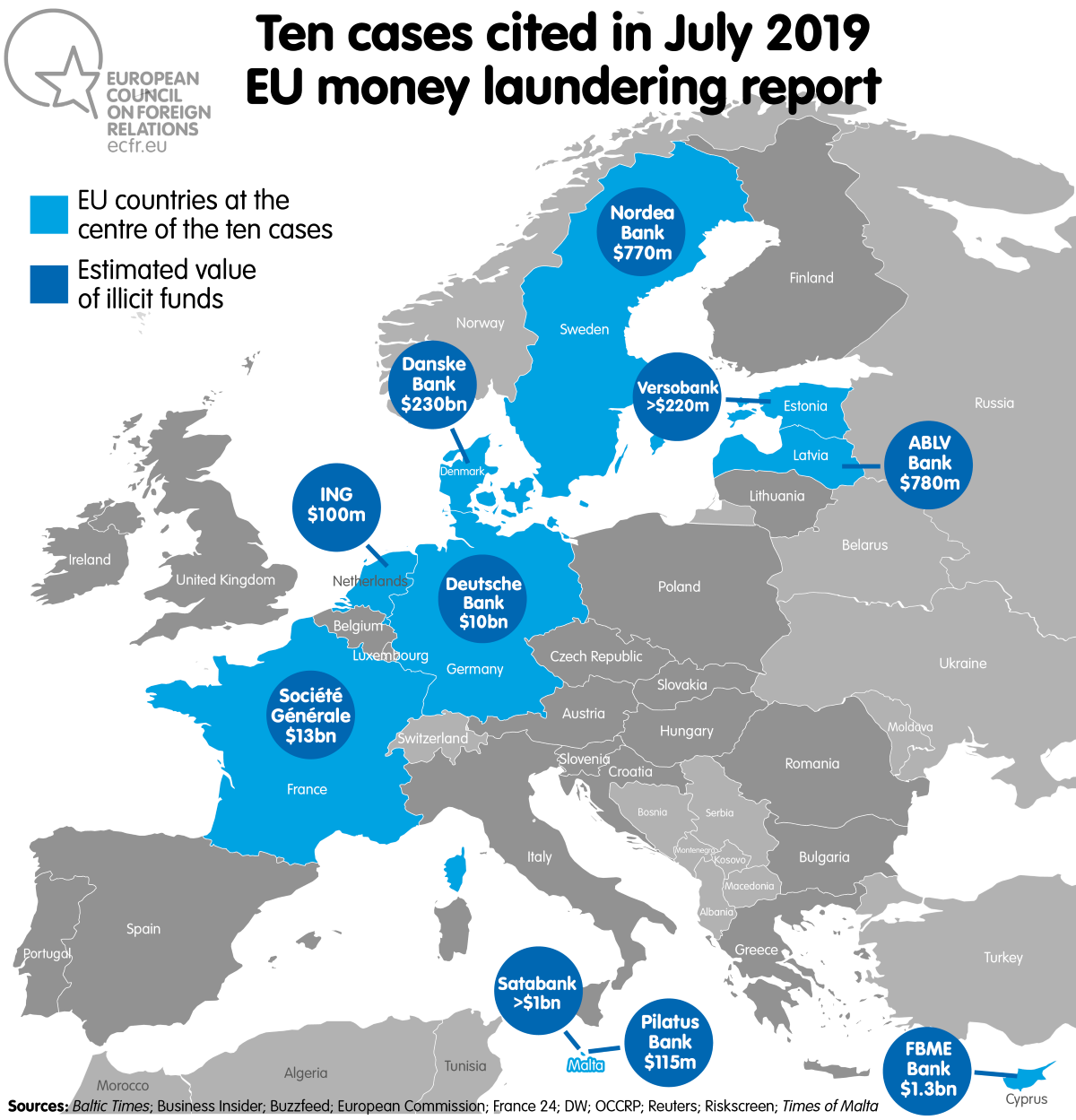

Kleptocrats and the networks they rely on often capture an influx of new resources when no government or outside power is willing and able to stop them. This can violently distort the local political economy, redistributing power in ways that compound security problems and societal breakdown. Europe, by providing a haven for plundered state funds, incentivises such behaviour – marring its efforts to create an international order based on the rule of law. The continent’s largest known money laundering scheme, the Danske Bank case, throws these dynamics into sharp relief.

Danske Bank and the destructive side of free capital movement

The Danske Bank case is stark reminder of how easily kleptocrats can capitalise on Western governments’ reluctance to inhibit the flow of money across national borders. As economists Dani Rodrik and Arvind Subramanian argue, powerful figures in many countries outside Europe “embraced financial globalization early on because they saw it as offering a useful escape route for their wealth”. Such figures were able to do so partly because “global financial elites had long relied on a [predominantly Western] narrative that equates capital controls with expropriation, and responsible policymakers did not want to be seen as violating property rights”. There are many such policymakers in Europe. And, where institutions fail to provide effective oversight of the international financial system, a policy commitment to the free movement of money across borders can have radical unintended effects.

This is apparent in the events that led to the closure of Danske Bank’s Estonian branch. Between 2007 and 2015, corrupt actors based in post-Soviet states allegedly laundered $230 billion through non-resident accounts at Danske Estonia, using shell companies and other firms in Spain, Sweden, the United Kingdom, and many other European countries. It was a profitable venture. In 2013 Danske Estonia had a return on allocated capital of 402 percent, compared to 7 percent across the bank as a whole. Yet regulators missed this and other signs that something was badly wrong. Three years earlier, Danske Estonia accounted for 30 percent of the country’s suspicious activity reports (which are a weak measure of risk individually, but a cause for concern in high numbers). Danske Bank’s finance director of several years went on to chair the Danish financial regulator from 2016 to 2018.

Much about the underlying nature of the Danske affair remains unclear. The purposes of many of the illicit transactions involved in the scandal have been lost to the grey, hazy world of cross-border financial crime. Even so, the case has had significant consequences: in 2019, the bank closed its branch in Estonia (on the orders of the country’s financial regulator) and announced that it would end its operations in Latvia, Lithuania, and Russia. The bank’s share price has fluctuated wildly during the scandal and its long aftermath, falling by around 50 percent between March 2018 and January 2019.

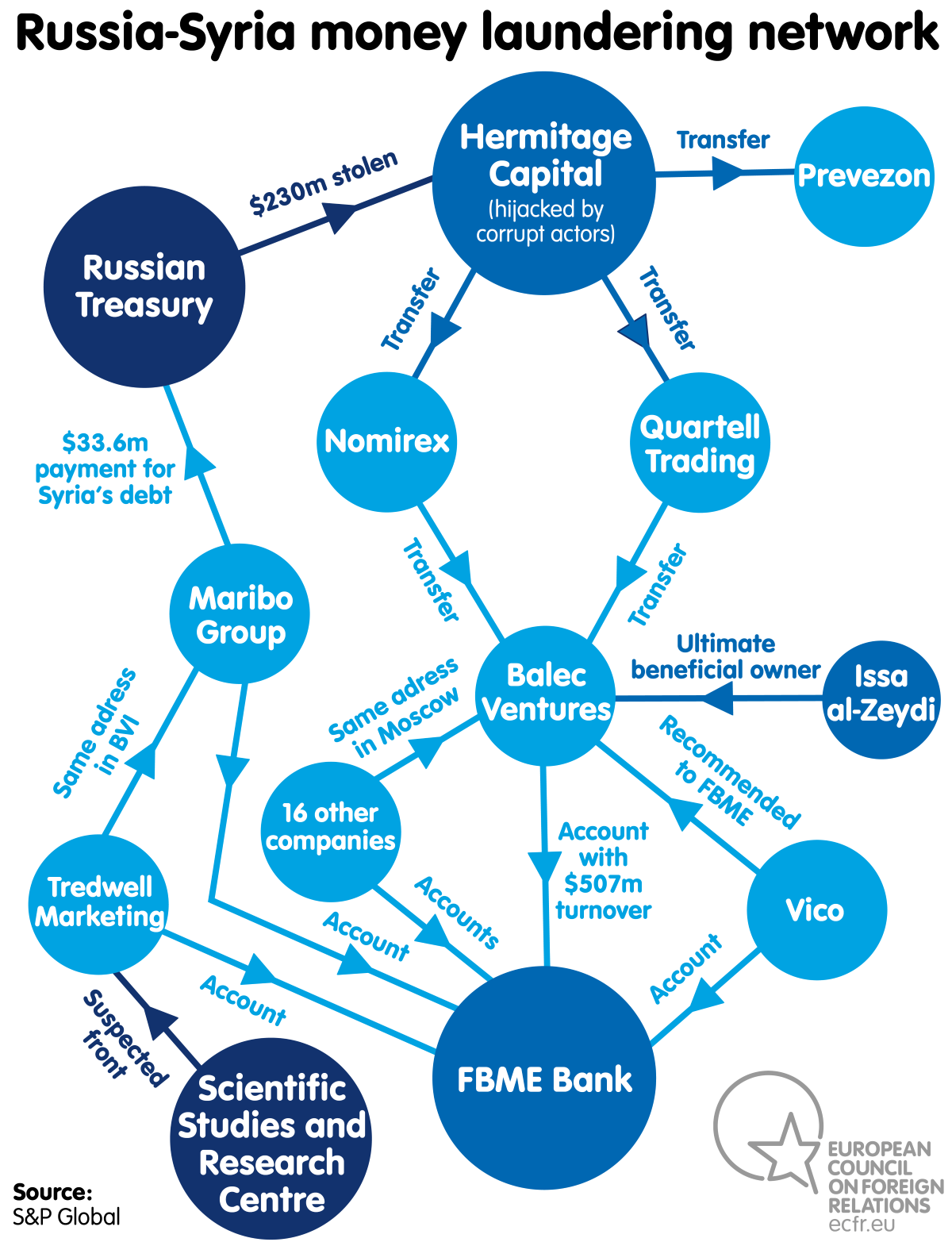

The Danske Bank case is connected to actors such as those behind the Russian Laundromat and the Azerbaijani Laundromat, which moved $2.9 billion in stolen funds through UK shell companies between 2012 and 2014. Perhaps the most troubling link in the case, though, is to the corruption network that killed Russian lawyer and auditor Sergei Magnitsky. In 2018 a report commissioned by Danske Bank revealed that its Estonian branch had received funds from a $230m tax fraud against Hermitage Capital Management, a crime Magnitsky investigated. The report neglects to mention Magnitsky himself – much less the fact that he was arrested for undertaking the investigation in 2008, or that he died in prison the following year seemingly due to inhumane treatment by the authorities, not least the denial of medical care. Nor does it refer to the perpetrators of the fraud, who appear to be corrupt officials within Russia’s bureaucracy and security services.

The Danske Bank report’s lack of curiosity obscures how kleptocrats exploit European financial networks to transform local corruption in Russia into a foreign policy problem that extends well beyond Russia’s borders. And the aftermath of the theft illustrates how kleptocrats often fund their international activities and pay off domestic allies. Danske Estonia is only one of several parts of the European financial system to be tainted by the Magnitsky case.

Some of the proceeds of the tax fraud moved through the Cyprus branch of Tanzanian bank FBME (formerly the Federal Bank of the Middle East). Investigations by the US Treasury and various private firms found that FBME acted as an indirect link between figures associated with the Russian government and the Syrian regime, through front companies such as Balec Ventures and Tredwell Marketing. The Financial Crimes Enforcement Network, part of the US Treasury, concluded that the bank helped transfer funds from the fraud against Hermitage to the Syrian regime’s Scientific Studies and Research Center, via a now-sanctioned Syrian-Russian frontman. In 2014 the US designated FBME as a financial institution of primary money laundering concern, leading to the bank’s closure three years later. For several years before the designation, European financial institutions such as Deutsche Bank, Commerzbank, and Raiffeisen Bank provided FBME with access to US dollars and the wider financial system through correspondent banking arrangements (which had fewer monitoring requirements than FBME’s direct relationships with its customers). There appears to be no evidence that these larger banks understood the types of activity that they facilitated through these arrangements – although that in itself raises questions about their fulfilment of ‘know your customer’ obligations.

In light of these failings, Magnitsky’s death seems all the more tragic for the importance of what he was trying to do. Although he could not have known it, at least some of the money from the tax fraud would, after passing through a labyrinth of European financial pathways, help fund an institution implicated in war crimes in Syria. As investigative journalists Irina Borogan and Andrei Soldatov contend, the “corrupt and cynical” system the Kremlin uses to enhance its influence at home and abroad has long exploited pliable foreign financial networks – and can trace many of its practices to the machinations of the Soviet-era KGB. The corruption networks that run through places such as FBME Cyprus help sustain an alliance between Damascus and Moscow that has endured since long before the fall of the Soviet Union. The klepintern, it seems, is alive and well. Grifters of the world, unite.

Given these events, European leaders who are uncertain about the severity of Europe’s money laundering problem might reflect on the Magnitsky case. They might also think back to an incident in which – having failed to destroy the financial networks that underpin the Syrian regime’s chemical weapons programme – France, the UK, and the US engaged in a form of enforcement that is far easier to understand (and probably much more expensive) than tortuous financial investigations. On the night of 14 April 2018, one week after the deaths of at least 40 people in a chlorine attack on Douma, the three countries launched more than 100 missiles at chemical-weapons facilities belonging to the Syrian regime. Their primary target was the Scientific Studies and Research Center.

How Europe became a major destination for kleptocrats’ money

A culture of light regulation

Such money laundering cases demonstrate how Europe’s channels of financial impunity benefit kleptocrats. As other European firms – including Nordea Bank and Swedbank – become caught up in similar allegations, the European Commission’s claim in July 2019 that the European Union “has developed a solid regulatory framework for preventing money laundering” seems increasingly hard to reconcile with reality. European voters, many of whom still live in the aftermath of the financial crisis, are entitled to ask why their governments have failed to prevent reckless behaviour by major banks in the past decade. To be sure, there are many differences between the problems that led to the crisis and those that lead to large-scale money laundering in Europe, but they are all mediated by the same political culture of undue deference to the financial sector.

In trying to understand Europe’s role in cross-border corruption networks, it is worth starting with the development of European attitudes towards financial regulation – and perhaps the unintended side-effects of the Maastricht Treaty. Economist Tamim Bayoumi shows in his analysis of the financial crisis that, “by hard-wiring regulatory competition [between member states] into the European financial system”, the treaty “reduced the incentives of European supervisors to look carefully at the behaviour of major domestic banks”. Each national regulator was reluctant to hamper its country’s largest financial institutions with rules more onerous than those in other member states. This sentiment combined with what economist Ashoka Mody describes as EU governments’ tendency to coddle leading banks, in the belief that doing so would drive economic growth. Bayoumi and historian Adam Tooze argue that a prevailing faith in market discipline to control financial risk-taking – akin to the libertarian ideology of former US Federal Reserve chair Alan Greenspan – helped deflect criticism of the system’s flaws. For years, a narrative that portrayed regulation as a barrier to economic efficiency and national competitiveness helped shield high-risk activity from scrutiny. If traders operating in licit markets could exploit a political culture that led to regulatory neglect, so could corruption networks intent on laundering money in Europe.

The greater financial supervisory role EU institutions took on following the crash has partially addressed the issue of competition between national regulators. Yet, while this may have established new checks on risky investments through measures such as increased capital buffers, it appears to have had little effect on Europe’s defences against money laundering networks. According to one attendee of a meeting of the European Banking Authority (EBA) in April 2019, the body chose to end its investigation of Danske Bank according to a logic of “let him who is without sin cast the first stone”. The EBA’s apparent approach to the decision suggests that a particularly destructive form of light regulation persists in European oversight of financial crime. Without a major shift in regulatory culture, kleptocratic networks will continue to have little trouble exploiting the boundaries between European countries as they move money into and across the bloc’s financial system.

However, European countries have become a haven for illicit wealth due not only to their regulatory failings but also to their robust laws on personal property. Kleptocrats who acquired their fortunes in jurisdictions where the rule of law is weak understand inherently the advantages of a strong legal regime. There is little point in stealing if one can be stolen from just as easily. By moving their illicit assets abroad, kleptocrats can gain legal protection for their wealth and cover it with a patina of legitimacy. This is part of the reason why disputes between current and former members of post-Soviet regimes so often play out in London courts. English common law provides the high degree of certainty about relationships between debtors and creditors sought by kleptocrats who have branched out beyond their home country.

EU member states may even contribute to this trend by selling citizenship. As recent investigations into “golden visas” found, some countries have sold EU citizenship to figures implicated in large-scale money laundering schemes, with little recourse to background checks. If European governments wish to preserve both their democratic institutions and the advantages of free capital movement, they should make a greater effort to secure this freedom with a broad defence of the rule of law – one that includes regulations strong enough to prevent kleptocrats from laundering money through the financial system.

However bleak the situation appears to be, endemic money laundering is not the unavoidable cost of doing business in European markets. Rather, it is the product of policy priorities, choices, and mistakes. Through a combination of political compulsion, ideological confusion, and wild optimism about the benefits of financial connectivity for long-term economic growth, European countries have too often empowered kleptocrats who share none of their love for democracy.

Entanglement with offshore havens

Regulatory issues aside, perhaps the most concerning aspect of Europe’s channels of financial impunity is their entanglement with offshore havens across the world. These jurisdictions – which are characterised by varying combinations of financial secrecy, light financial regulation, and low corporate taxes – have formed an important link in some of the largest money laundering schemes in Europe, including the Russian Laundromat.

At the core of offshore havens is a kind of collision between old and new. In his work on these jurisdictions, economist Gabriel Zucman describes how countries still rely on systems to register property that they created in the eighteenth and nineteenth centuries. Such systems are yet to fully adjust to the nature of the modern global economy, because they are a throwback to a time when financial assets and liabilities had a far smaller international role than they do today. Partly due to this mismatch, governments everywhere have allowed a great deal of wealth – especially that of the super-rich – to sit offshore, influencing the rest of the world in ways that are often hard to detect.

Drawing on research by the Bank for International Settlements, Zucman calculates that, by 2014, around $7.6 trillion – or 8 percent of global wealth – was held in tax havens. The figure breaks down into an estimated $6.1 trillion in securities and $1.5 trillion in bank deposits that had “no identifiable owners in global statistics”. (This includes only financial wealth and, therefore, excludes assets such as real estate and works of art owned through companies established in offshore havens – assets that corrupt actors often use to launder money.) Although the Organisation for Economic Cooperation and Development (OECD) introduced rules on international exchanges of financial information in 2009, the share of global wealth held in tax havens grew in the following five years. The share appeared to stay roughly the same between 2014 and 2017 – perhaps due to Western governments’ growing efforts during that period to counter tax avoidance and money laundering.

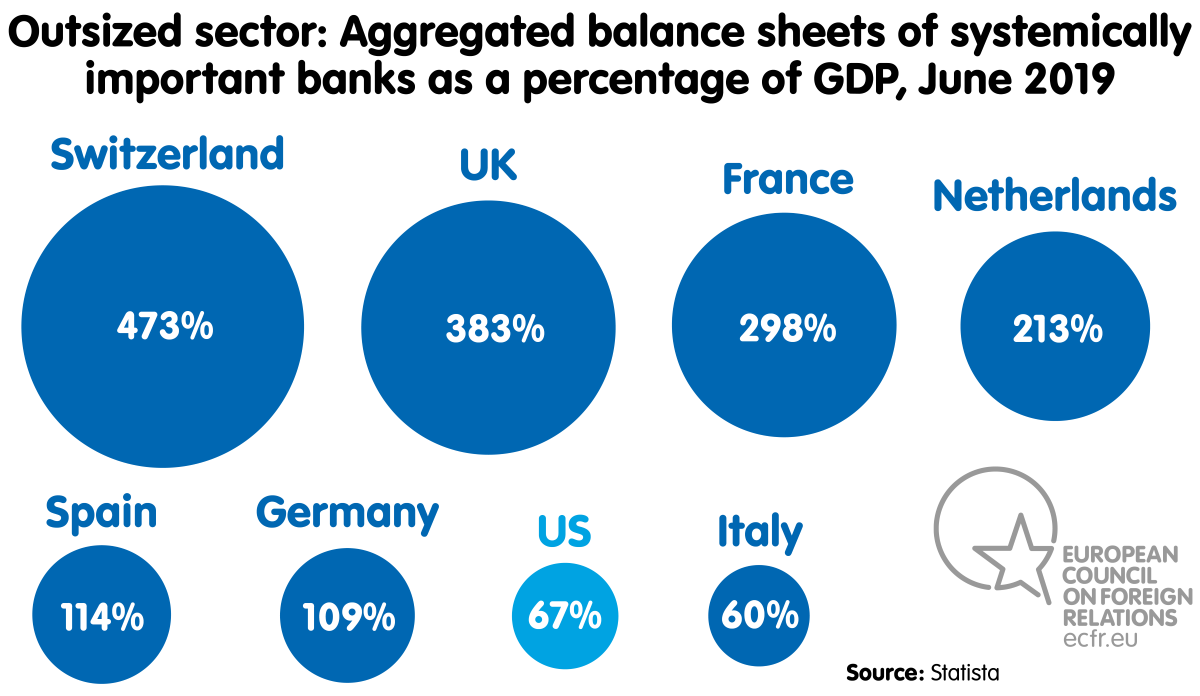

The UK and the US, home to the world’s two largest financial centres, have done much to build a global financial system in which offshore havens have an integral part. But European countries other than the UK have played a crucial role in this too. Banks based in France, Germany, the Netherlands, and Switzerland have, since the 1980s, made a huge contribution to the creation of the system – not least through acquisitions in the City of London and on Wall Street. The US may have forced Swiss banks to adopt greater transparency in recent years, but Switzerland is still one of the world’s leading providers of offshore financial secrecy.

The sheer number of scandals linking European giants such as Deutsche Bank, HSBC, and Société Générale to both kleptocratic regimes and offshore havens could suggest that money laundering through these jurisdictions is an inherent feature of globalisation. Indeed, the United Nations Office on Drugs and Crime reports that the prevalence of these havens – along with several other features of the global economy, such as a general trend towards financial deregulation – has made it increasingly difficult to identify and sanction criminal assets.

Equally, as political scientist Andrea Binder writes, offshore havens have long been important to international corporate and trade financing. For her, these entities are so integrated with the onshore economy that efforts to separate “dark money” from “clear money” create a false dichotomy. As a consequence, she argues, financial powers such as Germany and the UK “are now stuck with a system of offshore money creation that is at once indispensable and dysfunctional”.

Yet, if European governments are to pursue a foreign policy based on the rule of law, they cannot view the prevailing form of globalisation as unchangeable. While assessing the role of offshore havens in the broader economy, they will need to find new ways to distinguish between types of cross-border financial activity that are licit and illicit. They will also need to reckon with the fact that, as the International Monetary Fund (IMF) states, financial flows through these havens “greatly facilitate corruption” – even if most assets held there are likely unconnected to kleptocrats.

When they are well designed, policies targeting money laundering networks that depend on these havens can exploit the personalisation typical of kleptocratic regimes. Such personalisation is one of the greatest vulnerabilities of corrupt governments. By preventing kleptocrats from transforming illicit personal fortunes into offshore slush funds, European countries can limit hostile regimes’ access to resources and thereby shape their behaviour. For example, the US decision to sanction Latvia’s ABLV Bank in 2018 – which eventually led to the collapse of the firm – appears to have cut off at least one source of funding for the North Korean government. The potential influence of various Western countries’ far-reaching Magnitsky laws, and of measures introduced in response to the Panama Papers, is reflected in the furious response they provoke from the Kremlin and the Philippines government.

How kleptocrats’ financial activities disrupt European foreign policy

The ABLV saga was alarming but not unusual: the foreign policy challenges created by Europe’s channels of financial impunity grow by the year. And, at a time when the international environment is increasingly threatening to their values and interests, Europeans must, as Mark Leonard and Jeremy Shapiro put it, “address the interlinked security and economic challenges other powerful states present – without withdrawing their support for a rules-based order.” In this broad contest for influence, European states that seek every advantage should look to their underused power within the international financial system, especially the parts of it in which the rule of law no longer holds. Russia again provides a good example of why they should do so.

In pursuit of its foreign policy aims, the Russian government appears to have called on, or accepted the enterprising assistance of, members of the post-Soviet super-rich. As Kadri Liik explains, the Kremlin often makes use of “freelancers – be they criminal networks, activist oligarchs, or shady paramilitary units”. “While decision-making power is increasingly concentrated in the Presidential Administration”, she writes, “policy advice and execution often comes from sources outside established institutions, opening the door to various kinds of people who have unorthodox policy solutions.” This approach has been central to several high-profile operations in recent years, such as the coup attempt in Montenegro in 2016 (which was seemingly designed to prevent the country from joining NATO). As such, funds generated by corruption networks within Russia can, after passing through European financial institutions, support the country’s aggressive and disruptive policies abroad.

The movement of kleptocrat-linked money through the financial system has also had important implications for European foreign policy in states such as Ukraine. The country’s last pro-Kremlin president, Viktor Yanukovych, allegedly laundered the proceeds of bribery through banks in Sweden and other European states, providing him with hidden resources that likely enhanced his political power. His successor, Petro Poroshenko, allegedly continued to run a business empire while in office using companies in secrecy havens – a ruse that, when it came to light, arguably undermined public trust in the pro-EU government he led. Both episodes show how, as Gustav Gressel demonstrated for ECFR, Ukraine’s struggle against entrenched corruption has affected its geopolitical orientation. By facilitating such corruption, Europe has contributed to the instability that has plagued Ukraine for many years.

Poroshenko’s 2019 re-election campaign may have sunk beneath a wave of popular anger at elites, but oligarchic corruption continues to wear away at Ukraine – as it does Europe’s strategic and democratic-reform initiatives in the country. The case of PrivatBank illustrates the problem. In 2016, with the support of the Poroshenko administration, the Ukrainian central bank bailed out and nationalised PrivatBank at the cost of around $5.6 billion, claiming that the firm had engaged in “imprudent” lending practices. This was something of an understatement. A stress test reportedly discovered that the bank – which, with 20 million customers, was Ukraine’s largest – made 97 percent of its corporate loans to entities linked with its two main shareholders. As a subsequent investigation found, these two shareholders allegedly defrauded PrivatBank of around $5.5 billion, channelling the funds through a branch in Cyprus. The extraction of this amount of money, equal to the three-year loan the IMF negotiated with officials in Kyiv last December, undermined Western policy designed to stabilise Ukraine’s economy. The PrivatBank case indicates how, facilitated by corruption networks’ use of banks in Europe, narrow criminal entrepreneurship can transform into a strategic problem for European states.

Although it is hardly responsible for every instance of graft in Ukraine, the Kremlin has – as seen in the Yanukovych era – sometimes used corruption to force dependency on countries in its neighbourhood, aiming to dominate them politically. To an extent, the Kremlin has deployed corruption in modern-day Ukraine much as the British Empire deployed the opium trade in nineteenth-century China. Now, as then, an enfeebling addiction requires a supply line. The successors to the East India Company’s schooners and opium chests are shell companies and opaque bank accounts – many of them European.

Inadvertent maintenance of this supply line is only one of several financial mistakes Europe has made in countries affected by conflict. This can be seen in both Afghanistan and Iraq. As discussed earlier, one of the lessons of the wars there is that a large influx of European funding – public or private – into a fragile state can be counterproductive if it lacks support from exacting and enforceable anticorruption measures. Where there is no such oversight, and where access to money laundering networks in the West allows for large-scale theft with impunity, the consequences can be disastrous.

Chayes writes that, as Afghanistan’s corruption networks captured Western funding to expand their influence in the country, they subjected civilians to ever greater brutality. The cycle of abuse and disempowerment destabilised the aspiring democracy, tarnished public faith in the government, and increased support for the Taliban (which some Afghans saw as operating by a code, however brutal, that the authorities lacked). Partly as a result, even with thousands of troops on the ground, Western governments were never able to establish decisive leverage over the Karzai government or stabilise the country.

Western states’ flawed approach to corruption often combines with an inability or unwillingness to deal with local regimes based on a rigorous assessment of their past behaviour. Chayes repeatedly witnessed this problem in Western policymakers’ attitudes towards the Karzai government. Despite the fact that corrupt actors captured a great deal of Western aid to, and investment in, Afghanistan – or the fact that Karzai’s younger brother allegedly ran one of the most powerful criminal groups in the country – Western countries failed to recognise that the Karzai government’s “core activity was not in fact exercising the functions of state but rather extracting resources for personal gain”.

This dynamic also became apparent in Iraq, where similar problems shaped the relationship between Western capitals and the government in Baghdad under the leadership of Nouri al-Maliki. Long before he became prime minister, Iraqi officials and political parties set up hundreds of shell companies, creating cooperation agreements to capture lucrative government contracts. By 2006, the year Maliki took office, the special inspector general for Iraq reconstruction was already describing corruption as Iraq’s “second insurgency”. Tolerated and protected by Western powers, Maliki appeared to accelerate Iraq’s descent into kleptocracy. As prime minister, he oversaw the receipt of vast amounts of Western development aid and investment while allegedly hollowing out the state so severely that it would eventually pay the salaries of 50,000 soldiers who served only on paper, at the cost of at least $450m per year. By 2014, when the Islamic State group crossed the Syrian border and began its advance on Baghdad, politically protected actors appeared to have looted Iraq’s institutions to the point that the armed forces put up little resistance.

In this way, Europe’s complacency towards money laundering networks emanating from countries in conflict often subverted its development and investment programmes. At worst, rather than helping create democratic institutions or providing Western powers with leverage over the central government, these programmes had the opposite effect. Moreover, such failings likely undermined European voters’ support for international development funding.

Syria’s ultraviolent kleptocracy

Today, it is unclear whether Europe has begun to learn these lessons from the conflicts in Afghanistan and Iraq. In the past year, some European policymakers have called for the EU and its member states to begin funding reconstruction and other economic development in the parts of Syria controlled by the Assad regime. The outriders for this idea include noted champions of humanitarianism such as the Hungarian government. One foreign policy official in Brussels even claimed that “there’s a real opportunity to have some kind of leverage over how [the situation in Syria] pans out”.

The logic of such arguments is hard to follow. Europe can attach as many strict conditions to reconstruction funding in Syria as it likes, but it has no way to enforce them. The political and economic history of the conflicts in Afghanistan, Iraq, and many other places suggests that kleptocratic regimes cannot be tamed with largely uncontrolled flows of money (even where nominally pro-Western leaders control the central government). Instead, such funding often empowers corrupt actors to pursue their core economic and political goals – sometimes through the abuse of the European financial system – and to intensify their persecution of civilians.

By early 2019, the Syrian regime had conducted more than 320 confirmed chemical weapons attacks. Since then, it has continued to launch aerial bombardments of the two million civilians trapped in Idlib. There is no evidence that it intends to end its use of industrial-scale torture and rape to control dissent. Having waged a genocidal campaign for more than eight years, the Assad regime appears to be as committed as ever to governing “with the shoe over people’s heads”.

European leaders should judge the sincerity of the regime’s recent attempt to signal reform – the setting-up of a constitutional committee – by examining its past behaviour around ceasefire negotiations. They might be tempted to see a nascent anticorruption drive in its detention in 2019 of Rami Makhlouf, a cousin of the president who once controlled more than half of the Syrian economy. But, just as the Kremlin’s imprisonment of oligarch Mikhail Khodorkovsky in the early 2000s did little to defeat kleptocracy in Russia, such a move is unlikely to counter the entrenched corruption of the Assad regime.

As a 2019 investigation by the Financial Times shows, large-scale economic activity in Syria continues to be defined by proximity to the regime and its patronage networks. And the regime has long exploited the international financial system to support its war effort, far beyond the activities of the Scientific Studies and Research Center. Makhlouf featured in the Panama Papers and the Swiss Leaks, as well as a legal case that led the US Treasury Department to fine HSBC $1.9 billion in 2012.

Any European reconstruction or investment funds that entered Syria would have to avoid co-option by not only the regime, Russia, and Hizbullah – but also Iran. Another actor to feature heavily in the Panama Papers, Iran has been at the centre of recent money laundering and other financial crime cases that involve major European companies such as Crédit Agricole, Société Générale, and Standard Chartered. Elements within Iran’s state structures appear to be so reliant on international money laundering networks that, when the country’s foreign minister decried the situation in late 2018, some parliamentarians in Tehran called for his impeachment.

A number of European policymakers appear to hope to cut through all this to reform Syria, providing much of the estimated $250 billion-$400 billion required to reconstruct the country as an investment in stability. After years of failure to enforce the most important rule in any international rules-based order – the prohibition of genocide – they likely feel a need to be seen to be doing something. But whether they are motivated by humanitarian concern, diplomatic overconfidence, or self-interest (in encouraging refugee returns or winning lucrative construction contracts), they should try to learn from the failures of Europe’s past interactions with corrupt, abusive regimes.

The act of passing vast amounts of money to ultraviolent kleptocrats and their networks provides Europe with no leverage over them. Instead, it helps fund their campaigns to exact revenge on perceived rivals and secure political power at the expense of everyone else. Europe’s openness to illicit money only increases the likelihood of tragedy, as it provides kleptocrats with channels through which they can repurpose stolen investment and development funds. In this environment, it is far better to direct resources towards Syrians who live beyond the reach of the regime, where European policy can hope to establish a measure of genuine control. Having done little to mitigate the Syrian conflict, European countries can at least avoid funding the depredations of its main perpetrator.

How to counter kleptocrats’ use of illicit finance

Since the financial crisis, collaborative journalism – along with pressure from whistleblowers and civil society groups – has done much to heighten European governments’ awareness of kleptocracy, through investigations such as the Panama Papers. Work of this kind has led to, for instance, the resignation of a European prime minister, police raids on major European banks, and crisis meetings between national financial regulators. And shifts within global institutions may have also affected European governments’ attitudes towards corruption. For instance, the IMF has in recent years identified corruption as a significant threat to macroeconomic stability and a major source of public discontent, particularly among young people. Combined with an accelerating global campaign against tax avoidance, such developments have prompted several changes in policy that affect the flow of illicit funds through Europe.

In 2014 the OECD adopted the Common Reporting Standard – a measure that, geared towards tax compliance, promotes automatic exchanges of financial information between countries. In July 2019, the organisation stated that the value of bank deposits in tax havens had fallen by 20-25 percent, and that 90 jurisdictions had shared information on accounts that collectively held €4.9 trillion, since 2018. In 2016, perhaps realising that the standard signalled a shift in the mood, offshore centres such as Luxembourg and Switzerland began to disclose bilateral data (rather than aggregated data) on foreigners’ deposits in their banks. Meanwhile, the Financial Action Task Force, an intergovernmental organisation, has helped many countries counter financial crime through regular, if often flawed, assessments and recommendations.

The EU has created successive iterations of its Anti-Money Laundering Directive – and appears to be considering whether to replace these measures with harder-edged regulations. In 2019 the organisation pushed member states to comply with the directive, renewed its efforts to create a money laundering blacklist, and proposed the creation of an anti-money laundering enforcement agency. Countries such as France, Portugal, and the UK have recently experimented with freezing or seizing kleptocrats’ assets through the courts and the public prosecutor’s office.

Last year, the European Parliament adopted a resolution that called for an EU Magnitsky Act (in line with a Dutch proposal in November 2018), eventually prompting European foreign ministers to begin work on the initiative. In theory, the act will provide the EU with new powers to impose visa bans and asset freezes on foreign entities linked with corruption networks or human-rights violations. These entities could be included on blacklists that are, unlike most of the bloc’s sanctions, organised around themes rather than states – which allows for greater flexibility and precision in the selection of targets.

The implementation of Magnitsky-inspired national legislation in several European countries – Estonia, Kosovo, Latvia, Lithuania, and the UK – fits a pattern in which national governments have driven many of the most innovative anti-kleptocrat reforms of the past decade. Although politically protected corruption networks’ abuse of the financial system is a global problem, many of the major initiatives to counter it have come from individual countries.

For example, the US passed the Foreign Account Tax Compliance Act (FATCA) in 2010, the first Magnitsky Act in 2012, and the Global Magnitsky Act – which expands the scope of the legislation beyond Russia – in 2016. A blueprint for the Common Reporting Standard, FATCA formed part of the US campaign against Swiss banking secrecy. Similarly, the EU’s Fourth Anti-Money Laundering Directive drew on pioneering legislation on a fully transparent register of beneficial company ownership that the UK adopted in 2015.

Nonetheless, for all their promise, these American and British measures have so far fallen short of the combination of transparency, enforcement, and resourcing that democratic states need to prevent the rise of kleptocracy. FATCA effectively made US states such as Delaware and Nevada the most opaque secrecy havens in the world, because it left them with fewer requirements to exchange information on financial holdings than other territories. In parallel, the UK’s register has suffered from a severe lack of resources and, as such, verification and enforcement capability. While any member of the public can search for the ownership details of firms registered at Companies House, doing so reveals that more than 130,000 of them are formally controlled by people based in secrecy jurisdictions – and some by children under the age of two. Transparency on its own is not enough.

The Senate Banking Committee recently moved to address some of FATCA’s shortcomings with a bill that is as potentially valuable as an anticorruption measure as it is majestic a backronym: the Improving Laundering Laws and Increasing Comprehensive Information Tracking of Criminal Activity in Shell Holdings (ILLICIT CASH) Act. It is unclear whether the UK will follow suit by tackling its resourcing and enforcement problem, distracted as it is by Brexit. However, the US and the UK have demonstrated the value of ambitious national measures that could, with time and diplomatic pressure, form the core of an international coalition against kleptocracy.

Future policy

Given the extent to which the British and American financial and professional services industries have helped kleptocrats gain influence, the UK and the US have a responsibility to pioneer these kinds of far-reaching anticorruption policies. But their mistakes do not absolve others.

Partly due to the structures and ideologies discussed above, many European countries have fostered a culture of negligence towards corruption in the financial system. This culture sometimes appears to shape the complaints European leaders make about large American and, less often, British fines on European banks. Since the crisis, European countries have been repeatedly caught cold by US enforcement action such as the $8.9 billion fine on BNP Paribas in 2014 and the $7.2 billion fine on Deutsche Bank two years later. Although the US may have overreached in some cases, many European countries have simply declined to act.

These massive US fines are not the consequence of a plan to destabilise European finance hatched in Washington. They are the consequence of large-scale crimes. The global power of the dollar may allow the US to throw its weight around in ways that irritate European leaders but, in this area at least, they are lucky that it does so. Many European countries impose risibly small fines on misbehaving banks and, in some cases, even refuse to publish the details of these penalties. Either way, this builds up little deterrence against financial crime. If European leaders want to end US efforts to enforce the rule of law in Europe’s financial system, they need to take on the job themselves.

European countries have been decisive and innovative regulators in many other areas of the economy, such as environmental standards and data protection. And, in recent decades, they have increasingly used economic measures – particularly sanctions – as a primary mechanism for implementing foreign policy. With sustained effort and political will, they can draw on these experiences and capabilities to implement anti-kleptocrat policies that equal, or even surpass, those of the US.

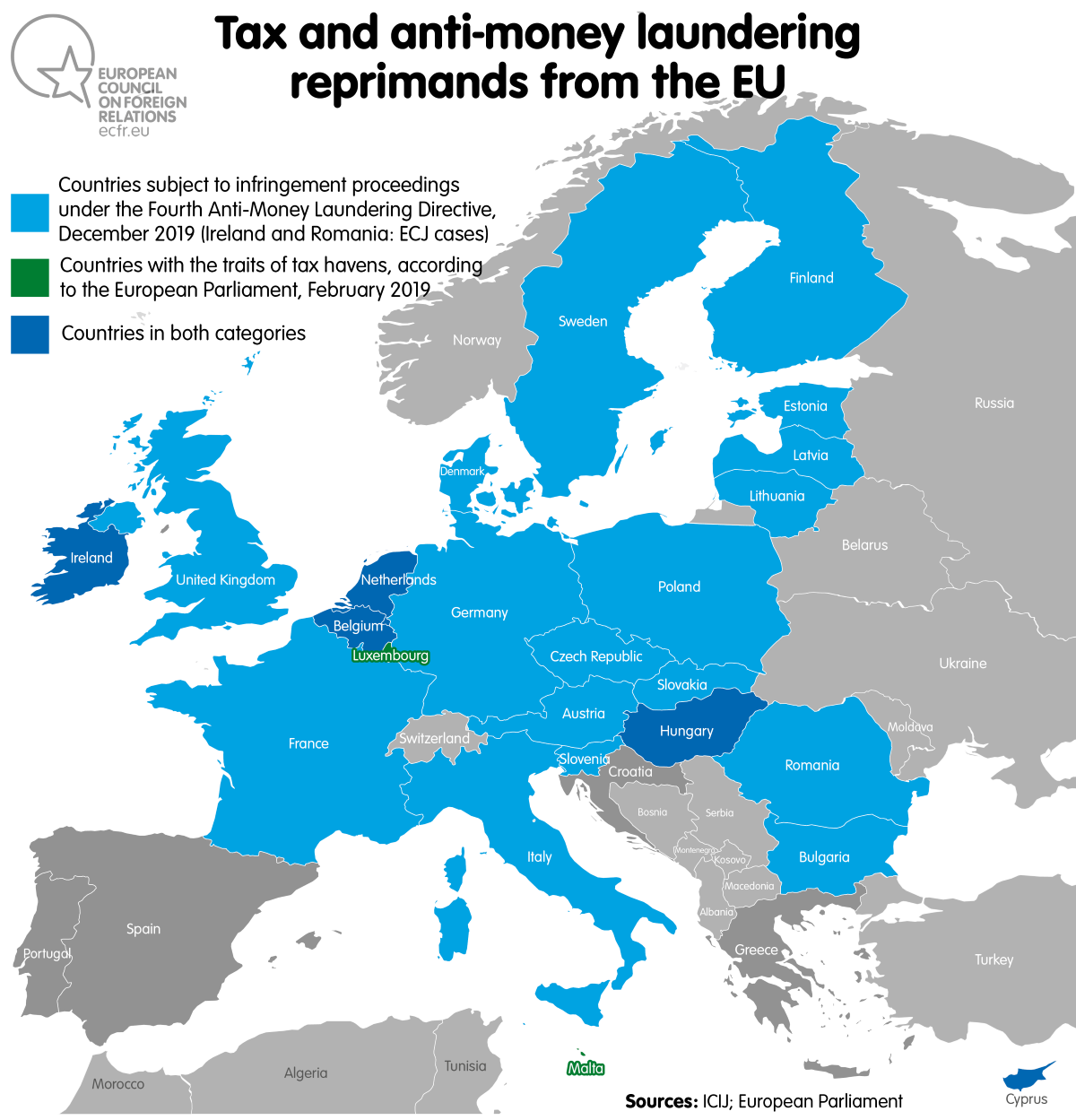

Nonetheless, as the European Parliament’s tax committee recently reported, many EU member states lack the political will to counter financial crime. And there are at least five other reasons why the bloc is unlikely to become a unified force against kleptocracy any time soon:

- According to the European Parliament’s tax committee, seven EU member states display the traits of tax havens. Any one of them could veto EU measures on financial secrecy that required unanimous support.

- Poland is – like Hungary, one of the alleged tax havens – no longer a full democracy. And EU institutions have found no way to change this. The Polish leadership could also block EU anti-kleptocrat measures that required unanimous support, if it believed that they posed a threat to its governance or economic model.

- Member states do not appear to agree on which kleptocratic regimes pose a threat to the EU. For instance, Nordic countries are far more sceptical of Russia and its intentions than Germany or Italy are.

- Due to their approaches to company finance, France and Germany are traditionally reluctant to make abrupt changes to banking regulations.

- The new European Commission initially nominated politicians who have been convicted of financial crimes to head two of the most powerful EU institutions. It also nominated a controversial member of the Hungarian government to lead the enlargement directorate-general (although the European Parliament rejected his candidacy). This signalled a lack of seriousness about deterring financial crime and upholding the rule of law more broadly.

Due to these political limitations, it is likely that some European countries will continue to express concern about the erosion of the international rules-based order but show little interest in enforcing such an order throughout their economies. The one redeeming feature of all this is that, if they can be made to recognise the severity of the threat from kleptocracy, it is within their power to do something about it. Countries that have the will to dismantle kleptocrats’ financial networks should take the following steps.

- Establish international transparency and enforcement mechanisms that end kleptocrats’ abuse of offshore havens. Building on the international campaign against tax avoidance, this effort should involve the creation of coalitions with non-EU financial powers such as the US and the UK. It should work towards creating, as Zucman recommends, a global register of financial wealth.

- Develop rigorous threat assessments designed to prevent European initiatives from funding kleptocrats and their networks, particularly figures implicated in war crimes and crimes against humanity. This should involve analysis of the behavioural history of abusive regimes, as well as the history of European states’ interactions with kleptocrats in earlier conflicts. It should sometimes lead to the redirection of European funding away from environments in which Europe has no real control.

- Constrain kleptocrats’ enablers in Europe through reform of laws and enforcement practices covering the financial and professional services industries (not least the legal, accounting, public relations, private intelligence, and property sectors). This effort should focus on issues such as corporate liability, campaign funding, whistleblowers, libel, and lobbying. It should also address the dangers of regulatory capture highlighted by the Danske Bank case.

- Assess major banks’ contribution to the European economy in relation to the societal and political damage caused by endemic money laundering. As part of this, European governments should commission independent economists to identify areas in which light financial regulation and the free movement of capital have strengthened or weakened the productive economy.

- Create public trusts to fund the work of investigative journalism cooperatives and civil society groups that focus on corruption. These organisations have often identified threats from foreign-based kleptocrats where the state has failed to do so – yet many of them appear to rely on private donors.

- Conduct social research into public attitudes towards kleptocracy and measures to counter it. An ECFR study published in April 2019 concluded that, “dyed-in-the-wool party voters are a thing of the past, and today’s European voters – who have a strong concern about corruption – place more emphasis on the integrity of political leaders.” If they are to counter the threat from kleptocracy, European leaders will need to do so in a way that garners public support. It remains unclear whether European voters strongly oppose foreign-based corruption or understand its links to the erosion of the rule of law in their own economies.

To develop and monitor these initiatives, countries that have the will to dismantle kleptocrats’ financial networks should establish government institutions dedicated to countering kleptocracy. These institutions should draw together specialists in criminal and international law, law enforcement, intelligence, economics (particularly finance), foreign policy, and even history. And they should regularly liaise with investigative journalists and civil society groups.

Anticorruption strategies and plans are useful as declarations of intent and snapshots of a point in time, but Europe’s best hope for countering kleptocracy comes from the kind of continual adaptation and reassessment found in a living institution. This is the flexible culture and practice that dedicated anti-kleptocracy bodies should aim to foster. Such institutions would have the depth of expertise needed to understand and start to offset one of the great strengths of resilient kleptocratic regimes: the capacity to bend all elements of the state, the private sector, the media, and the criminal underworld to their core objectives of regime survival, self-enrichment, and revenge.

European governments may be reluctant to implement some of these measures due to fear that new limits on free capital movement or financial creativity will damage the European project and their interests at home or abroad. Yet freedom without the rule of law is just anarchy.

About the author

Chris Raggett is an editor at the European Council on Foreign Relations. He previously worked as an associate editor at the International Institute for Strategic Studies, as well as for a legal publisher and a medical journal.

Acknowledgements

The author would like to thank Jeremy Shapiro for his ideas on restructuring the paper and support in publishing it, as well as Adam Harrison for his assiduous editing. He would also like to thank Vessela Tcherneva and Peter Pomerantsev for their insightful reviews of an earlier draft. They all improved the paper immensely.

The European Council on Foreign Relations does not take collective positions. ECFR publications only represent the views of their individual authors.