Blue China: Navigating the Maritime Silk Road to Europe

Senior Policy Fellow

Summary

- China’s Maritime Silk Road is about power and international influence, but Europeans should not overlook the importance for China of further developing its blue economy, which already represents 10 percent of China’s GDP.

- The Maritime Silk Road already affects Europe in five main areas: maritime trade, shipbuilding, emerging growth niches in the blue economy, the global presence of the Chinese navy, and the competition for international influence.

- On balance, the Maritime Silk Road creates more competition in Europe-China relations, but it also creates space for cooperation in the blue economy and for specific maritime security missions.

- Europe should emulate China’s blue economy as an engine of growth and wealth, and encourage innovation to respond to well-funded Chinese industrial and R&D policies.

- Europeans should strengthen their contribution to maintaining a strategic balance in the Indo-Pacific region and uphold their vision of a rules-based maritime order.

Introduction

“If you want to be rich, build a road first” (要想富,先修路). There is rarely a conversation about Xi Jinping’s Belt and Road Initiative (BRI) – his plan for greater connectivity for China across both land and sea – in which this six-character proverb does not crop up. But in the shape of the Maritime Silk Road part of the strategy, the route exists already and is vital to China’s ever-growing wealth. The sea lanes of communication from China to Europe through the Malacca-Suez route are among the busiest in the world. Twenty-five percent of world trade passes through the Malacca Strait alone. China-Europe maritime trade is three times larger than trade by air freight and Eurasian railways, while the last alternative – the Northern Route through the Arctic Ocean, that China dubs the “Ice Silk Road” – is only just starting to develop.

But China intends to go much further down this road, almost literally. The State Oceanic Administration (SOA) – the lead agency developing policy on the blue economy (蓝色经济) – defines the 21st century as “the century of oceans: the status of oceans in national development dominates more than in any other period of human history”.[1] Its 2017 annual Ocean Development Report reported that China’s “marine GDP” (including marine industries, exploitation of ocean resources, and services such as tourism and transport) represented 9.5 percent of its total GDP in 2016.[2] If it was a country, at more than $1,000 billion China’s blue economy would rank 15th in the world by GDP.

This figure alone should convince Europeans to pay more attention to China’s activity at sea. But its ambitions are set to ramp up even further. The Maritime Silk Road is about the next phase of developing the country’s blue economy; it rebrands existing maritime policies already promoted by the SOA and the National Development and Reform Commission (NDRC) and directs investment towards key sectors and to intensify maritime trade. By doing so, their growth prospects grow from merely regional to global. The keywords for China’s future blue economy are ‘technological innovation’ and ‘global leadership’.

Economics may be its main driver, but the Maritime Silk Road is also about naval power and international influence and forms part of Xi Jinping’s broader national strategy. In his work report to the nineteenth party congress, the Chinese president stated that by 2050 China will have “become a global leader in terms of composite national strength and international influence”.[3] Maritime policies play an important role in support of that strategy. At the eighteenth party congress, China elevated the “construction of a strong maritime country” (海洋强国 ) to the level of national goal for the very first time. With the nineteenth party congress, Xi Jinping’s second term opened with an indication that maritime policies are fully a part of his global leadership ambitions. As a result, the People’s Daily now publishes opinion pieces from leading officers at the Academy of Military Science advocating the need for stronger naval power in order to allow for an “expansion of strategic space” at sea, an argument which only a few years ago would not won endorsement from the party’s most official media outlet.[4] After constitutional amendments putting an end to the two-term limit for China’s presidency adopted in February 2018, it is certain that Xi Jinping will stay in power beyond 2022 to make these ambitions a reality. The plan is written in black and white in his work report to the party congress. At no point in the post-Mao era have Chinese ambitions been so clear. And the maritime domain is central to this.

Besides the blue economy and naval power, the Maritime Silk Road is also about addressing what Chinese intellectuals have described for many years as a deficit of “power of discourse” (话语权 ) – the ability of states to impose their concepts, ideas, and narratives and to shape international discussions. By playing on the mythical appeal of the ancient route that first emerged during the Song dynasty, China seeks to promote an attractive narrative in international politics. The Maritime Silk Road therefore comes with a major public diplomacy push.

Xi Jinping launched the Maritime Silk Road initiative during a visit to Indonesia in November 2013. Five years on, this policy paper reviews what China has already achieved and highlights the maritime areas where China is set to grow in importance in the next five years. The paper focuses on the main corridor of the Maritime Silk Road – the Malacca/Suez route through the Indian Ocean – where European interests are more immediate and bigger than on the nascent “Ice Silk Road” and the Oceania-South Pacific Blue Economic Passage, which connects China to Australia. The Maritime Silk Road is indeed about power and influence. But Europeans should not overlook the importance of the blue economy for China, and they should not dismiss the Maritime Silk Road as mere propaganda. In fact, Chinese actions already affect European interests, in five main areas:

- Maritime trade

- Shipbuilding

- Emerging growth niches in the blue economy

- The global presence of the Chinese navy

- Geopolitics and the global competition for influence

The report concludes that, on balance, the Maritime Silk Road creates more competition than cooperation opportunities in Europe-China relations, including on a fundamental level – the very terms of engagement in Europe-China relations. Competition is inevitable but Chinese actions also create space for cooperation in the blue economy and for specific maritime security missions. These opportunities should not be missed – but a clear mind is needed regarding Chinese power ambitions.

1. Europe and the Maritime Silk Road: engaging on Chinese terms

The romance of the Silk Road has won over few players in western Europe. In early 2018, ahead of visits to China, both Emmanuel Macron and Theresa May declined to sign a memorandum of understanding on Maritime Silk Road with the Chinese government. Such a move would have formally endorsed the Chinese initiative and provided a loose, albeit non-binding, political commitment to cooperate on specific projects. Macron stated that “these roads cannot be those of a new hegemony, which would transform those that they cross into vassals”.[5] The Financial Times reported that Downing Street did not bend despite persistent pressure from the Chinese to sign.[6] German foreign minister Sigmar Gabriel went even further in criticising the BRI as seeking to promote “a comprehensive system alternative to the Western one, which, unlike our model, is not based on freedom, democracy and individual human rights.”[7]

Similar scepticism exists across Europe and at the level of the European Union itself. While China’s May 2017 Silk Road Summit in Beijing heard opening addresses from Vladimir Putin and Recep Tayyip Erdogan, European presence at the event was very low-key. Only one head of state – the Czech president, Milos Zeman, and five heads of government (of Greece, Hungary, Italy, Poland, and Spain) attended. European representatives refused to sign a Chinese-introduced statement on connectivity and trade because of a lack of references to social norms and transparency standards; as a result the statement was not adopted.[8] The German economy minister commented that Europe’s demands on “free trade, setting a level playing field and equal conditions were not met”.[9] Back in Europe, the European Commission is currently preparing policy guidelines to set out European terms of engagement for connectivity projects – a set of norms and rules, and a response to the BRI. In short, a reluctance to accept Chinese terms of engagement on BRI projects dominates the European debate and is mainstream at the level of the EU.

How to explain this outcome, given the intense Chinese public diplomacy campaign? First, China’s narrative stressing shared prosperity has failed to convince. The BRI is essentially viewed in Europe as a geopolitical project about power and influence. Chinese insistence that the project is not a “strategy” has not only fallen on deaf ears, it has been counterproductive. In July 2016 China suddenly began promoting the term “initiative” to put an end to the international use of the “One Belt One Road strategy”. But by doing so it only reinforced the association of the BRI with a strategic dimension. Second, there is a sense that Europe does not have much to gain from the Maritime Silk Road, except for investment in port infrastructure that will only exceptionally constitute game-changers for the foreign relations of the recipient country. And European companies are real alternatives to Chinese investment, as shown by the recent privatisation of the port of Thessaloniki, sold to a consortium of French, German, and Russo-Greek companies for €1.1bn.[10] Outside Europe, in the words of one European diplomat, reacting to data released by the Center for Strategic and International Studies, “if more than 90 percent of BRI-related contracts go to Chinese firms, our firms compete with the rest of the world for the remaining 10 percent – this is not a significant market”.[11] Third, Europe is divided over BRI. There is tension between business interests in several EU member states seeking deals with China in the blue economy and more protective forces that focus on the potential risks of Chinese investment in terms of political ramifications and Europe’s long-term competitiveness. The result is that passive scepticism has gained the upper hand. The alternative – enthusiastic endorsement – would need a clear majority or a positive consensus that is nowhere to be found.

Is such scepticism deserved? There is no question that the BRI is designed to help China tilt the global balance of power in its favour. Xi Jinping is outspoken about his ambitions. His work report to the party congress provides a clear roadmap and a timeline to reach goals defined in terms of global leadership by 2050. Foreign minister Wang Yi describes the work report as “not only a program of action for the CPC, but also the most authoritative textbook to understand and approach China”.[12] This is the meaning of the “new era of socialism with Chinese characteristics” (新时代中国特色社会主义 ), the key concept of the work report. Many in the Chinese strategic community understand it as the beginning of a new three-decade period: under Mao, China stood up and recovered sovereignty (中国站起来了 ); under Deng and his successors, national strategy was about “getting richer” (富起来 ); in the new era, China seeks power and influence on the international stage (强起来 ).[13] The BRI matters enormously to this goal, as a key instrument of China’s grand strategy that coordinates the mobilisation of “an extensive array of national resources in pursuit of an overarching political objective”.[14] In the words of a Chinese scholar, the BRI is not only a “key priority of great power diplomacy with Chinese characteristics” (中国特色大国外交的重中之重), it also helps achieve the goal of a “rational adjustment of the international order” (国际秩序理性调整 ).[15]

The Maritime Silk Road should be understood in this context as an essential strategic tool for Xi Jinping’s goal of turning China into a “strong maritime country”. According to the SOA’s think-tank, the China Institute for Marine Affairs, a strong maritime country means: a developed blue economy, strong innovation capacity in maritime science and technology; success in protecting the maritime environment; and a powerful navy.[16]

Of these four goals, the blue economy is a matrix for the other three. Focusing too much on geopolitics risks overlooking the strategic value of the blue economy. In the language of the SOA and the NDRC, the ministry-level agency that conceives and oversees China’s five-year plans: “the eighteenth Party Congress made the important strategic decision to build a strong maritime country, stimulate the growth of the marine economy, and expand the space for the engine of blue growth, which are important for realising the Chinese dream of rejuvenating the Chinese nation and reaching the goal of the ‘two centenaries’”.[17] From the perspective of these two institutions, the Maritime Silk Road is about helping implement the country’s thirteenth five-year plan (2016-20) in the maritime domain.

In practice, the blue engine matters in three ways. First, the SOA and NDRC define some industries of the blue economy as “strategic”, and these will thus receive priority in decisions about state support. The March 2016 document issued by the SOA and the NDRC details the implementation of the 13th five-year plan in the blue economy by listing key strategic sectors.[18] The targets include upgrading traditional marine industries (fisheries, shipbuilding, and offshore oil and gas exploitation), supporting emerging strategic industries (maritime engineering, maritime biology pharmacy, renewable energies, and sea water utilisation) and developing a modern maritime services industry: coastal and sea tourism, public transport, and maritime finance. All these industries are likely to benefit from a ‘Silk Road effect’ and register solid growth over the duration of the thirteenth five-year plan and beyond.

This realistic assessment of Chinese strategic ambitions in the blue economy does not mean that no cooperation opportunities exist for Europe or that European actors will not survive increased competition. China’s “Vision for Maritime Cooperation under the BRI”, a document issued by the SOA and NDRC in 2017, outlines marine ecological conservation, blue carbon, customs cooperation, and marine research infrastructure as key areas for international cooperation. European public and private actors that can negotiate advantageous terms with Chinese counterparts may be able to benefit from partnerships.[19]

In addition, a pure focus on geopolitics results in overlooking the domestic dimension of the Maritime Silk Road. The State Council, China’s government under the leadership of the Communist Party, has a different perspective. The Silk Road is one of “three great national strategies” (三大战略) to reshape China’s economic geography, alongside the Beijing-Tianjin-Hebei integration plan and the green development of the Yangzi River Economic Belt.[20] The 2017 vision document on maritime cooperation issued by the SOA and NDRC details the regions that can leverage their strength under the Maritime Silk Road: the Bohai Rim, the Yangzi River Delta, Fujian, the Pearl River Delta, and coastal port cities. It also cites local plans such as the Zhejiang Marine Economy Development Zone, the Fujian Marine Economic Pilot Zone, the Zhoushan Archipelago New Area, and efforts to promote Hainan Province as an international tourism island.[21] Coastal provinces make up 14 percent of Chinese land but host 40 percent of the population, more than 60 percent of the country’s GDP, and 90 percent of its foreign trade, including more than 70 percent of energy imports.[22] They have been the main winners of China’s economic boom, and the Maritime Silk Road is a sign of political support for the next phase of their development in the blue economy, a major source of wealth, and a promising area of growth.

Chinese analysts systematically downplay the link between China’s blue economy and Xi Jinping’s plan for global leadership. They concede that investment leads to influence but tend to reject the notion that this is the primary intention. “Of course, if China has successful relations alongside OBOR, it will extend Chinese influence; but this is not the objective of the original project.”[23] They usually present influence as a side benefit of economic projects. “We develop stronger economic ties with many countries, we build infrastructure which boosts our exports, which we need. We also build friendships. But we do not care about political systems. We are not interested in alliances, nor in security involvement.”[24] Since the nineteenth party congress, Xi Jinping has insisted that China has no intention of exporting its political system.[25] However, even if it was unintentional, China has provided an option for all political forces rejecting democratic values, and on the domestic front it has articulated a narrative about the superiority of the Chinese model which it promotes relentlessly.[26] This should be sufficient to conclude that, from the Chinese perspective, there is an ideological competition with the liberal model that China intends to win.

The blue economy matters hugely for China’s development – the Maritime Silk Road is not an empty slogan merely seeking a low-cost way to change perceptions of China, or to act as a cover for global naval power projection. In fact, several important projects are already in train, and more are coming. In the wise words of one Beijing-based analyst, “The new Silk Road does not mean there will be many new projects; it is more about incrementally increasing engagement and about consistence of cooperation. … Port infrastructure is key to but not the total of the Silk Road project. We upgrade our existing economic engagement and pursue the next wave of globalisation.”[27] What matters is how these existing projects change China’s political relations with recipient states, deepen the importance of China as a global maritime player, and create new incentives for a more interventionist foreign policy.

Understanding the big picture is not straightforward. China’s insistence on abstract principles such as “win-win” and the “Silk Road spirit” defined as “peace and cooperation, openness and inclusiveness, mutual learning and mutual benefit” tends to blur the factual reality on the ground.[28] For analysts, understanding the level of strategic design as opposed to actual projects is challenging because flagship projects are in diverse states of progress – container traffic at the port of Piraeus is booming, while Kyaupkyu in Myanmar is still stuck on the drawing board. According to the SOA, the Maritime Silk Road entered the implementation phase only in 2015, with 2016 the “key year” when central and the local government began to treat the project as a priority.[29] The next five years will see more action – and more pushback – from China’s rivals, it says.

It is also notable that infrastructure building as a foreign policy tool is not a new phenomenon for China – the link between regional transport networks and strategic influence was already clear a decade ago.[30] But the Silk Road brings this approach to a whole new level. In sum, China has a roadmap with clear priorities. The Maritime Silk Road reflects China’s ambitions in the blue economy and should be treated as such. But it is a political project rebranding existing economic policies to have them serve a national goal articulated with clarity in Xi Jinping’s report to the nineteenth party congress – leadership status in world politics. Continuous growth in the blue economy will be supported by the build-up of the country’s naval power and will accompany the ongoing adjustment of China’s security posture from a regional to a global scale.

2. Five key implications for Europe

2. 1 Maritime trade: China’s increasing global footprint

Maritime trade is the lifeblood of EU-China economic relations. In 2016, 64 percent of EU-China trade in goods (in volume) was transported by sea, as against 2.06 percent by rail, 6.35 percent by road, and 27.59 percent by air. This corresponds to €315 billion. These percentages stayed stable in 2017 – maritime trade still represented 63.66 percent of the total during the first 10 months of 2017.[31] The supremacy of maritime trade is not even threatened by new China-Europe trains. These may capture the imagination, but the day they compete with ships is far off. In early 2018, the cost of shipping a container by sea from Shanghai on the European route was 797 USD if the final destination is a Mediterranean port and 912 USD if the destination is further north.[32]

By contrast, while the cost for Chinese companies to ship by train to Europe through Russia is around $1,000 per container, it is artificially maintained at that level thanks to heavy subsidies by Chinese local authorities, which comply with policy instructions from the top – incentives are estimated to range from $1,000-5,000 per 40-foot container.[33] Trains occupy specific niches: delivery of goods to landlocked regions, goods for which exact delivery time matters or goods that need a stable temperature such as pharmaceutical products. The fact that trains take between 16 and 20 days while ships need between 35 and 50 days matters much less than predictability of arrival time. But this advantage is offset by a major weakness. Trains face a problem of traffic congestion at transit points on the eastern and western borders of Russia when transshipment occurs between different gauge systems.

The supremacy of ships may be virtually unchallenged, but from a Chinese corporate perspective, there is a question mark over the long-term profitability of shipping as a core business activity. Operating port terminals is a source of predictable and stable return on investment for Chinese conglomerates, unlike shipping, which depends on oil prices. As a result there is an incentive for Chinese state-owned enterprises (SOEs) to expand into business areas surrounding shipping, including investing in port infrastructure and other logistical components of maritime trade. One article notes that the decrease in shipping costs has only a marginal impact on trade, and, as a result, shipping companies need measures to ensure that their shipping business can survive – port management and alliances are particularly important.[34]

Indeed, an important shift is already taking place. Xu Lirong, chairman and party secretary of COSCO Shipping since 2013, not only expects his company’s investment in the port terminal business to significantly increase in the coming years and become an important source of growth, he also makes the important point that the terminal business is more stable and often more profitable than shipping, because it has “a fixed rate of return on investment, which can be between 8 percent and 10 percent, even up to 10 percent”. As a result, he presents the rebalance of the company’s activities towards seeking more profits from the terminal business as a necessary adjustment that is also “helpful for China” as the country develops “important strategic channels”.[35]

Creating the conditions for continuous growth in EU-China maritime trade is in the interests of Europe, but Chinese investment in port infrastructure along the Maritime Silk Road is not without risks for recipient countries. In a positive scenario, such Chinese investment would reduce the cost of trade for all parties. But in a negative scenario, Chinese conglomerates would be in position to set prices and dictate the terms of economic exchanges to trade partners.

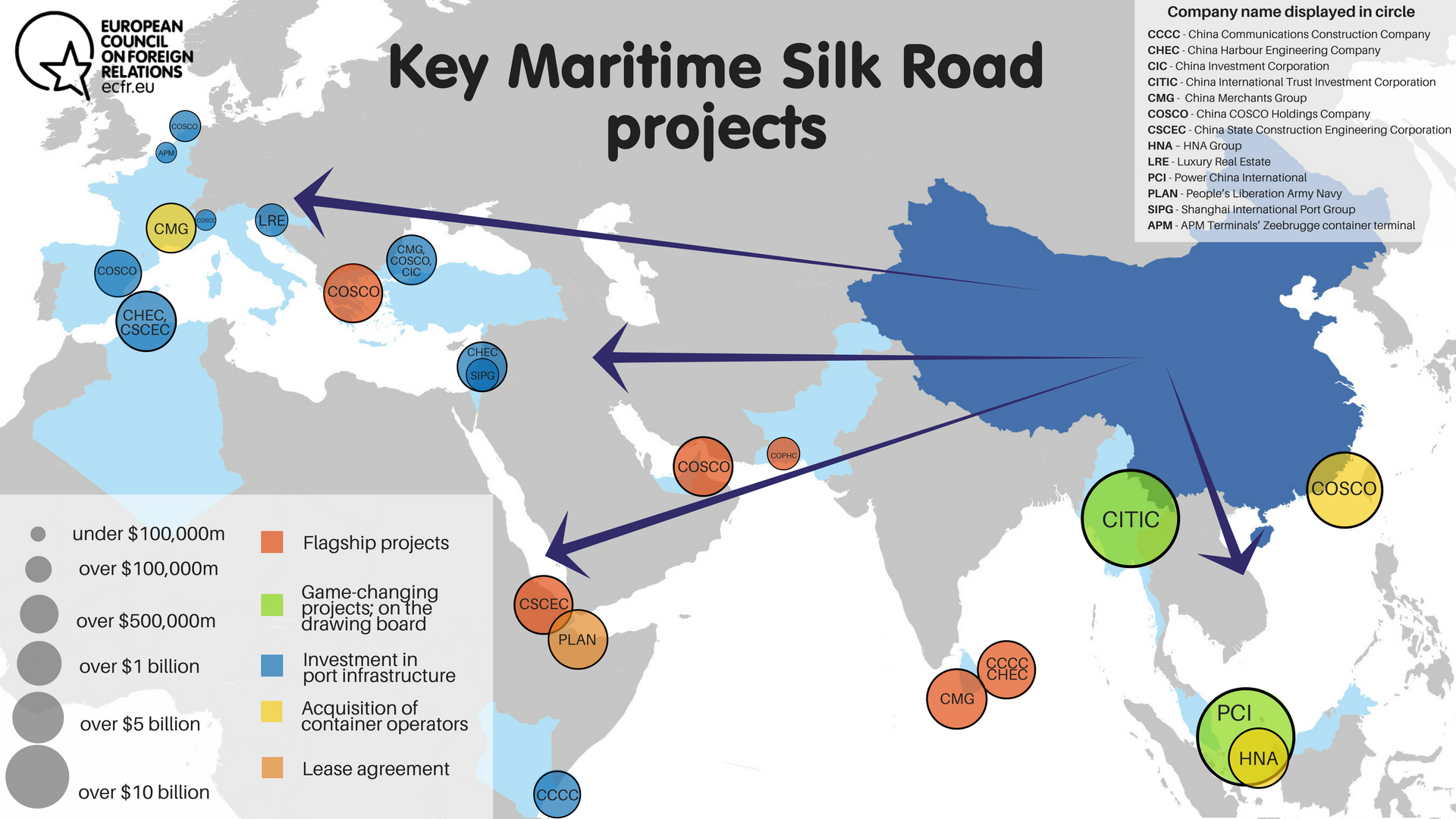

Concretely, today the Maritime Silk Road consists of a set of flagship projects in port infrastructure, financial investment in port management, and acquisitions of container management companies across Europe, the MENA region, and east Africa. The map shows the state of play of actual investment, including for projects that are still on the drawing board. As Thierry Pairault shows in a study on port terminals operated by China, a port area is primarily a space where private industrial and commercial activities are carried out. The port authority retains the land ownership and the country its full sovereignty. The port authority concedes a terminal to an operator – in this case Chinese – which operates the container terminals by signing concessions that entail no transfer of ownership. Five Chinese companies are among the world’s leading port operators: Hutchison Ports (HPH), COSCO Ports, China Merchants Ports (CMP), Shanghai International Port Group (SIPG), and Qingdao Port International (QGGJ). All these companies are present in the major ports along the MSR, with a marked preference for European ports, in Greece, Italy, France, Spain, Belgium and the Netherlands. Chinese companies are also present in Turkey, Israel, Egypt and Morocco.[36]

The perspective of the SOA is different. It notes that only 25 percent of China’s trade is transported by Chinese companies, which suffer from low competitiveness in the high-end service industry – the whole sector is big, but not strong (大而不强 ).[37] But both large corporations and the SOA think in terms of catching up and long-term competitiveness.

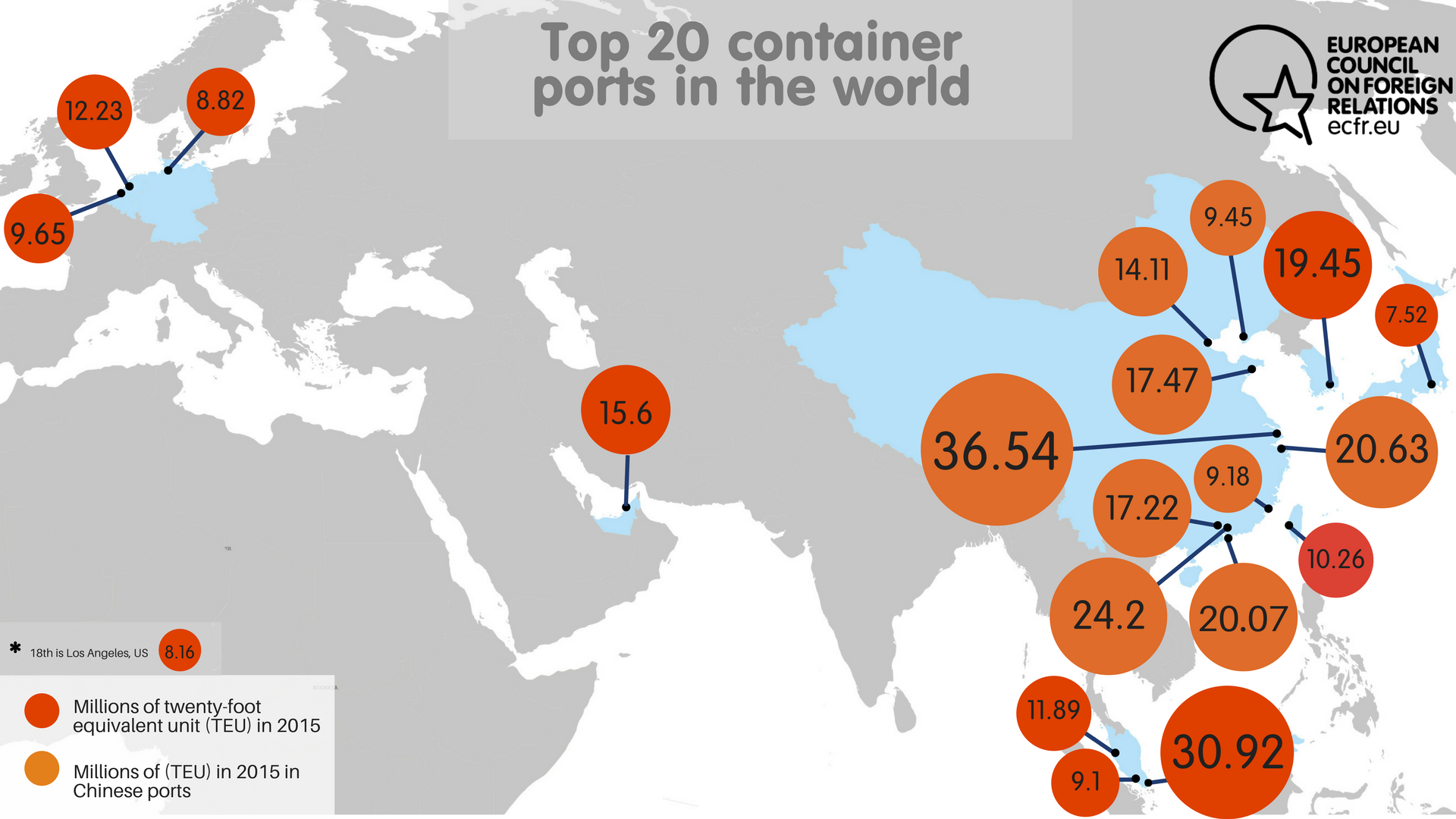

So far, five flagship port projects dominate the landscape because of their scale, their relative political importance for China’s relations with the recipient state, and because they go beyond being simply holding stock investments but include either building or extending infrastructure: Piraeus in Greece, Hambantota and Colombo Port City in Sri Lanka, Gwadar in Pakistan, and Djibouti. Each story is unique but they share similarities. All five spearhead a wider strategy to accumulate investment from other large Chinese corporations. Port infrastructure is a vehicle for deeper penetration of local markets – some would say “market creation” for Chinese companies. Hambantota, Gwadar, and Djibouti all include plans to create free-trade zones. Piraeus comes with investment in the tourism sector in Greece. All five include plans, at different stages of implementation, for additional investment in the transport sector: railways, airports, roads, and new flight routes for Chinese airlines. In sum, port infrastructure encapsulates China Incorporated in action. However, actual maritime trade varies considerably from port to port. At one extreme, Gwadar does not have a container terminal yet, and at this stage remains a small cargo port only poorly connected to its hinterland.[38] In Djibouti, the base has barracks and defensive features, but does not yet have a pier for naval ships.[39] At the other extreme, Piraeus’s container traffic grew by 14.4 percent in 2016 and COSCO plans to turn it into the fifth largest European port for container traffic (it was eighth in 2016 and not in the top 15 in 2007).[40] The Greek shipping minister Panayiotis Kouroumblis has described Piraeus as “evidence that the Silk Road is progressing” while COSCO’s main Piraeus chief executive Fu Chengqiu announced that “the dream of becoming one of the biggest ports in the Mediterranean with 10 million TEU [twenty-foot equivalent unit] annual capacity will come true soon”.[41]

Large-scale ports are never simply a story of economic development. They have been a source of controversy, facing opposition from in Greece and in Sri Lanka (popular demonstrations against the takeover in both countries) and even terrorist attacks targeting Chinese nationals in Pakistan connected with the Gwadar project. For all governments, choosing Chinese investment in infrastructure projects is a major foreign policy decision. For Greece, doing so was at least in part a response to the EU’s austerity measures; Sri Lanka and Pakistan court China as part of their policy towards India; Djibouti gains the leverage to negotiate basing rights with other partners. Inevitably, by inviting Chinese investment in large-scale infrastructure, these countries also accept Chinese political influence. Greece became the first country to break ranks with the EU at the United Nations Human Rights Council when it refused to support an annual resolution whose language on China the Greek foreign minister described as “unconstructive criticism”.[42] Projects in Sri Lanka have given rise to “debt-trap diplomacy”, a term coined by Indian scholar Brahma Chellaney to describe how a new democratically elected leader no longer has the option to significantly review contract terms signed by their predecessor, as the contracted debt deprives them of leverage.[43] The 2017 debt-for-equity swap on Hambantota is indeed a powerful example of a large infrastructure project leading to a narrowing of political options for an indebted government.

Besides these flagship projects, two in south-east Asia deserve special mention, as they could also change the nature of China’s relations with the recipient states if they reach agreement on financing and practical modalities: Kyaupkyu in Myanmar and Malacca Gateway in Malaysia. These are divisive issues in these two countries and are likely to remain so for the foreseeable future. But, at the same time, Chinese companies have made concrete moves of a smaller scale. In 2016 and 2017 there was a sudden rise in Chinese purchases of stakes in port management worldwide, with occasional investment in infrastructure upgrades and rarely a management concession agreement – but mostly financial investment. They included four acquisitions by COSCO in Noatum Ports in Spain (which operates container terminals in Valencia and Bilbao), Rotterdam container terminal in the Netherlands, Khalifa Port in Abu Dhabi, and Vado Ligure in Italy.

There are also clear signs that more acquisitions in Europe are set to follow in port management. China Merchants Group has designs on cities on the Arctic shipping route (Kirkenes in Norway, Klaipeda in Lithuania, and ports in Iceland). Other ports that have a registered Chinese interest include Elefisna in Greece, Trieste and Genoa in Italy, Sines and Lisbon in Portugal, and Anaklia in Georgia. Some plans will necessarily fail. In early 2018, China Communications Construction Group withdrew a bid to build a deep sea port on the Baltic Sea in Lykesil, in Sweden, after 3,000 people signed a petition raising environmental and security concerns.[44]

What are the implications for Europe?

- On the positive side, new and upgraded infrastructure can reduce transaction costs. For recipient states, new infrastructure means economies of scale and a “dramatic reduction of freight costs”, as explained by the chief executive of Abu Dhabi Ports, Captain Mohammad Juma Al Shamisi.[45]

- Local concerns around the political ramifications of such decisions are real, as the Piraeus case shows. They arise from a general problem with an emerging pattern of investment which may lead to undue political influence. The analysis above makes clear that profit drove the recent acquisition decisions made by COSCO and China Merchants Group. As central SOEs, their leadership is nominated by the Communist Party and they receive targets from SASAC, but they are much more than simply implementation units of the Politburo’s Standing Committee.[46]

- There is a catching-up angle to Chinese investment in ports. In the words of the SOA, “Port service industries are mainly based on handling services. Comprehensive logistics services still lag behind international advanced ports such as Rotterdam and Singapore. Although the scale of China’s development of resources keeps extending, the capacity to provide added-value products and services still lags behind.”[47]

- There are no restrictions in Chinese regulations specific to foreign investment in the blue economy, except for water transport companies and ocean shipping tally. The 2017 catalogue on foreign investment moved the marine transport service industry from the “restricted” to the “authorised” category, specifically referencing the Maritime Silk Road.[48] The problem for Europe is less with individual regulations than about asymmetry in the way Chinese central SOEs operate in comparison with European firms. There is also a general problem with the lack of reciprocity between the EU and China on access to public procurement contracts, which has implications for Europe-China relations in the blue economy.[49]

- Over the long term, the risk for Europe and other players is that they will face Chinese companies which are setting prices and controlling the terms of exchange. This a long game and it remains the case that the two largest shipping companies in the world – Maersk and MSC – remain European. But control of port infrastructure offers a strategic advantage in terms of selecting business partners.

2.2 The risk of slow death for the European shipbuilding industry

A key turning point in China’s policy under Xi Jinping has been the adoption of a national development strategy centring on innovation – how to move from catching up to shaping global technological change. This change features in many policy documents, the most significant being the “Innovation Driven Development Strategy”, adopted in 2016 by the Central Committee and the State Council. It sets the goal of becoming an innovative country by 2020, move into the top tier in the ranking of innovative countries by 2030-35, and attaining global leadership by 2050. [50] These goals mirror the roadmap outlined by Xi Jinping in his 2017 work report to the party congress.

This ambition has direct implications for the shipbuilding sector. Marine engineering and high-tech shipping are one of the 10 priorities in the “Made in China 2025” industrial innovation plan. Future high-tech ships are required to incorporate new information technologies together with a propulsion system emitting less carbon. Indigenous innovation must be achieved by raising R&D spending levels through centres of excellence. According to the SOA, this is necessary given that the rise in labour costs is making China’s comparative advantage vis-à-vis Japan and South Korea disappear.[51]

Despite being the world’s number one shipbuilder in 2017 in three categories (completion of ships, new orders, and volume of holding orders), China still lags behind Japan, South Korea, the United States, and Europe in the categories of high-value ships and related high-end marine technologies.[52] Those include LNG vessels (methane and gas carriers), scientific vessels, military vessels and associated technologies. The Chinese shipbuilding industry has long been characterised by low added value, a weak independent design capability, and a lack of synergy. In the main it has built unsophisticated vessels like oil tankers, cargo and bulk carriers and, more recently, container ships, categories which are very exposed to the fluctuations of the world economy. In 2013, high-value LNG vessels and marine engineering platforms represented only about 7 percent of all the profits made by the Chinese shipbuilding industry. Italy’s Fincantieri, Germany’s Meyer Werft, and France’s STX still hold a technological advantage in the construction of high-value ships in the very specific niche of the cruise ship market. This advantage helped revive the shipbuilding sector in Europe. China, like Europe, is also embarking on the development of new technologies for offshore oil and gas exploitation as well as renewable and clean energies.

At the eighteenth party congress, the Central Committee set out a blueprint for the strategic transformation of the shipbuilding industry. Facing a major crisis in the shipbuilding sector caused by the post-2008 slowdown of the world economy, in 2013 the State Council took a series of drastic measures to support the industry and reorientate it towards more profitable “high tech” and “high value” vessels and technologies. It enacted the “Implementation plan for accelerating the structural adjustment of and promoting the transformation and upgrading of the shipbuilding industry (2013-2015)”, extending until the end of 2015 an earlier policy of retiring or upgrading old transport vessels and single-hull tankers.[53] Shortly after, the State Council published its “Guiding opinions on solving the serious problem of over-production capacity”, noting that only 75 percent of the shipbuilding industry was being used. The Ministry of Industry and Information Technologies then issued its “Shipbuilding Industry Regulatory Requirements” (船舶行业规范条件) to accelerate its restructuring and downsizing. A “white list” of 51 shipbuilding companies was declared to be in line with the new requirements and to qualify for bank credits and government financial support.[54] The rest of the sector is left to survive on its own and is actually at risk of complete disappearance

Chinese plans for high-value ships, including cruise ships, will inevitably threaten the European cruise ship industry – that is to say, most of Europe’s commercial shipbuilding. Today, Europe dominates the global market. In June 2017, 74 luxury cruise ships were ordered to be built in 19 shipyards across the world, including 27 orders with Fincantieri (in six shipyards), 19 orders with Meyer Werft in two shipyards, and seven with STX France.[55] Fincantieri’s decision to assist China’s CSSC Baoshan shipyard with the construction of two VISTA Class cruise ships (with an option for four more) has all the appearances of a bid for very short-term profit for itself. More importantly, the move will end up helping to create a Chinese competitor and ultimately give the coup de grace to the European cruise ship industry, whose best growth prospect is, in fact, the Chinese domestic market.

Fincantieri was forced into this association by its main customer – Carnival, the US owner of Costa cruise – striking a deal with China to extend its operations in mainland China provided that it builds its new cruise ships in China. BRI-related communications now frame it as an Italian contribution to the project, but the cruise ship technology transfer to Baoshan will endanger not only Fincantieri’s own future in the cruise ship market, it will also damage the prospects of the other European builders, including Fincantieri’s new site in Saint-Nazaire (the former STX France), and its German rival Meyer Werft with its three yards in Papenburg and Rostock in Germany, and Turku in Finland. In 2016, Genting Hong Kong completed the acquisition of Nordic Yards’ three shipyards in Wismar, Warnemunde and Stralsund, Germany, for about €230.6m. The acquisition will add to Genting’s expertise in building cruise ships for its three customers Crystal Cruises, Dream Cruises, and Star Cruises.[56] Meanwhile, the Swedish and Swiss company ABB is helping China enter the ferry ship market in Europe by providing automated systems to vessels built in China. Scheduled for delivery in 2020, a 13-deck, 2,800-passenger capacity Chinese-built ferry will connect the Finnish port of Turku to Stockholm in Sweden.[57] Meyer has already expressed its concern over the technology transfer to China.

In this context, the temporary nationalisation of STX France by the French government in 2017 is one of the first examples of European resistance to technology transfers that undermine long-term competitiveness. STX has a €4.5 billion contract to build four World Class luxury cruise ships, to be delivered to MSC Cruises between 2020 and 2026. The World Class is characterised by liquefied gas propulsion that ensures no carbon emission.[58] The language that the French government used to explain the unusual nationalisation decision cited the risk of technology transfer to China through Fincantieri, given the latter’s joint venture with China State Shipbuilding Corporation.[59] The story reached a conclusion at the end of 2017 when France authorised the Italian takeover of STX following the signature of an agreement between Fincantieri and the French industrial conglomerate Naval Group to consolidate the European shipbuilding industry in the military sector.[60] Fincantieri’s argument that the group is moving to the next generation of propulsion was not a sufficient safeguard for the French government. Overall, surviving Chinese competition will remain an arduous task, given the size of China’s domestic market. On the European market, there will still be space to favour European domestic shipbuilders through regulatory measures, linked, for example, to environmental standards.

The cruise ship market is not the only niche where China is threatening Europe’s shipbuilding advantage. With its unprecedented quantitative and qualitative naval build-up, China has made remarkable technological progress that now allows its products to compete in parts of the military sector which European shipbuilders previously dominated. In the surface vessels market, China has exported frigates and corvettes to Thailand, Pakistan, and Malaysia – which used to be customers for new or second-hand Western platforms – and to Algeria, which traditionally bought its platforms from Italian, British, German, and Soviet/Russian builders. While Chinese naval exports of minor craft to sub-Saharan countries date from the cold war years, its recent success in selling two offshore patrol vessels to Nigeria was made at the expense of more traditional German, British, or French suppliers to that country. Besides the transfer of second-hand vessels (including submarines) to Myanmar and Bangladesh, two countries with limited resources which never constituted a market for European builders, the sale of Chinese submarines to both Pakistan and Thailand took place at the expense of France’s former DCNS and Germany’s HDW/TKMS. Lower costs and political leverage have played in China’s favour. But it is also a fact that European exporters can count less and less on their quality advantage, even in Latin America, which has weaker ties with China. With China currently demonstrating its capacity to build an aircraft carrier, France’s hopes of selling a carrier design to Brazil in the coming decade will have to take into consideration Beijing as a credible competitor. Another effect of China becoming a competitor for the export of advanced systems is the need for European producers to move up the ladder of technology transfers to satisfy customers – a recent example is the French transfer of nuclear attack submarine technology to Brazil, but without the nuclear reactor.[61]

With global demand for energy rising, the development of offshore oil and gas and the demand for offshore oil and gas platforms has increased significantly. According to China’s Marine Economic Bulletin, the added value of the offshore oil and gas industry and its share in the marine economy doubled from 74.8 billion yuan, accounting for 5.8 percent in 2010, to 157 billion yuan, accounting for 7.6 percent in 2012.[62] Both the added value of the offshore oil and gas industry and its share in the marine economy have surpassed that of the shipbuilding industry.

At the eighteenth party congress, the Central Committee set out its plans for the development of the marine energy sector through oil and gas exploration, marine wind power generation, and ocean wave power generation. China’s subsequent offshore engineering equipment construction activity follows the principles of achieving self-reliance, assimilating and improving foreign technologies before attempting to export them to foreign markets. The oil field service of China National Offshore Oil Company (CNOOC) consists of four business modules: geophysical prospection, drilling, oil field technology, and specialised vessels. And its international influence keeps rising. The China Oil Field Service Limited (COSL) is a subsidiary of CNOOC with overseas branches in Singapore, Dubai, the US (Houston), and Norway. The shipbuilding industry designs and builds offshore oil and gas platforms for shallow and deep water (60-160 metres in length), production storage vessels (FPSO) displacing 50,000 to 300,000 tons, and deep semi-submersible drilling platforms (500-3,000 metres).

However, at present, China does not yet have a complete R&D and industrial chain production for offshore equipment. From a global perspective, the competitiveness of the domestic offshore industry is still weak. The cost of the imported equipment is much higher than that of the Chinese-made hull on which it is installed. The latter represents only 20 percent of the price tag of a large FPSO or a large semi-submersible platform valued at several hundred million US dollars. Industry research institutes have undertaken national research projects and have been supplying equipment for land-based oil fields for many years. Home-produced equipment for the offshore industry will be available once technical obstacles are overcome. The shipbuilding industry has made significant progress in the field of unmanned submersibles, manned submersibles, and multipurpose project ships. To reduce duplication, Chinese commentators call for the shipbuilding industry to open its research facilities up to the offshore industry, especially its specialised laboratories for testing marine equipment (reliability testing laboratories, special meteorology laboratories, electromagnetic compatibility testing rooms, marine anti-corrosion anti-fouling test sites).[63]

Marine renewable energy is key for raising the percentage of clean energy and constructing a low-carbon system. Offshore marine energies, especially wind farming, have the potential to minimise the land use requirements of the power sector and reduce greenhouse gas emissions. As of 2017, all the biggest offshore wind farms are in northern Europe. The 630-megawatt London Array in the UK is the largest, and it is set to be followed by even bigger projects at Dogger Bank, Norfolk Bank, and the Irish Sea. Likewise, China’s industrial and economically developed coastal areas have great demand for electricity. Beijing has identified using marine wind energy and speeding up the development of offshore wind power as a means to solve the energy shortage in the coastal areas. It encourages China’s shipbuilding industry to contribute to the offshore wind power industry by using its turbines and diesel technologies as well as its gearboxes, anti-corrosion anti-fouling research and treatment, and its blade design. Tidal current energy, temperature difference energy, and wave energy are also valuable new avenues both for Europe and China. Near-shore reserves of temperature difference energy are huge in the South China Sea where there is a strong incentive to develop the technology. In Europe, France’s Naval Group is a leader in the field, advertising its technology to Chinese neighbours like Indonesia.

Fincantieri’s and Nordic Yards’ decisions to cooperate with China reflect the freedom of economic actors in a sector, the cruise ship market, which the SOA and NDRC identified as a key priority for China’s shipbuilding industry. In order for its shipbuilding, offshore, and energy sectors to survive, Europe must find ways to preserve its niches of expertise through innovation and technological advantage. With Beijing’s new emphasis on science and technology, this task will become more and more difficult.

2. 3 Towards Chinese leadership in emerging strategic industries

Science and technology are a priority for the development of China’s blue economy. Many official documents make clear that while the current phase is to catch up to reach the level of advanced countries, the next phase is about global leadership. While developing the Made in China 2025 plan for high-tech ships, the SOA emphasises the technologies that will support the exploration and the exploitation of maritime resources, with a particular focus on deep sea resources – the new frontier of the global marine economy. To support deep water oil and gas exploitation, several categories of ship will receive additional R&D support: maritime research ships, geophysical vessels, half-submerged oil drilling platforms, deep water working stations and berthing systems, and ocean polar research stations. The SOA emphasises the importance of developing deep water space stations and large floating structures.

China is engaged in a comprehensive effort to support the exploration of maritime resources, particularly in the case of deep sea resources, to which the SOA gives special political attention and constant emphasis.[64] China is one of only 20 states to have signed contracts with the International Seabed Authority (ISA) to explore poly-metallic nodules, sulphides, and cobalt-rich ferromanganese crust, through the SOE China Minmetals Corporation and China Ocean Mineral Resources Research and Development Association in several authorised areas in the Pacific Ocean and the Indian Ocean. China has invested in shipbuilding to carry out this ambitious plan, and is building the first deep sea mining vessel.[65]

There is a consciousness among Chinese maritime security analyst that technological breakthrough may change not only the balance of power, but also the balance between competition and cooperation in China’s foreign relations in the maritime domain. In the words of one senior analyst reflecting on the first successful exploitation of methane hydrate in the South China Sea in the deep-sea belt at 1,266m below sea, once China masters the technology, “other countries will be more interested in cooperating with us”.[66]

The existence of mineral deposits in the deepest parts of the ocean has been known of since the mid-nineteenth century. The volcanically formed hydrothermal sulphides on the seabed contain copper, zinc, and precious metals including gold and silver. The first calls for exploitation were made a century later by the US, prompting the United Nations to adopt a regulation system under the ISA, the intergovernmental organisation established by the UN Convention on the Law of the Sea (UNCLOS). As the world’s largest consumer and importer of minerals and metals, China is now developing the technologies for mining these deposits.

Since 2001, Beijing has applied to establish for four mineral resources exploration zones in the international seabed area. Asked about China’s plan a scientist at the SOA explains that Beijing’s activities will actually depend on commodity prices as well as the state of the technology.[67] China is acting with the blessing of other countries under exploration contracts awarded by the ISA. In 2001, the China’s Ocean Mineral Resources Research and Development Association won exclusive exploration rights for the 75,000 square kilometre polymetallic nodules in the Clarion-Clipperton zone in the middle of the eastern Pacific, and preferential development rights for when the polymetallic nodules enter into commercial development.[68] The UK – through a partnership between the government and a subsidiary of Lockheed Martin UK – has also received a permit to explore a segment of the Clarion-Clipperton Zone. In July 2011, China’s Ocean Mineral Resource Research and Development Association achieved exclusive exploration rights and preferential development rights for the polymetallic sulphites in the 10,000 square kilometre seabed field in the south-west Indian Ocean. Under the arrangements, 15 years after the signature of the contract, China will abandon 75 percent of the area and keep 25,000 square kilometres as a field with preferential developmental rights. In July 2013, authorised by the ISA, China’s Ocean Association received exclusive exploration rights and preferential developmental rights in the 3,000 square kilometre cobalt-rich mine in the north-west Pacific Ocean. Similarly, fifteen years after the signature of the contract China will abandon at least two-thirds of the area and eventually keep the exploration rights of 1,000 square kilometres. In July 2015, China Min Metals Corporation achieved an exclusive exploration development rights of the polymetallic nodule resources in the Clarion-Clipperton zone.[69]

In January 2017, Poland applied for the 29th exploration contract, following other European countries like France, Germany, the UK, alongside India, Japan, South Korea, Russia, and the lnteroceanmetal Joint Organization (a consortium of Bulgaria, Cuba, the Czech Republic, Poland, Russia, and Slovakia). Contracts have also gone to a growing cohort of private entities sponsored by both developed and developing states. Using technologies developed by UK-based Soil Machine Dynamics, Nautilus Minerals is planning full-scale undersea excavation of mineral deposits off Papua New Guinea. However, a dispute with the government delayed production. Canadian and EU experts working under the MIDAS project assessed the Nautilus Minerals project as posing risks for the environment.[70] This issue will be key to the future of deep sea mining, including Chinese ventures which remain under the supervision of the ISA. Indirectly, the EU assessments on the ecological viability of deep sea mining may influence the future of China’s ambitious projects.[71]

It is not yet known whether undersea excavation of mineral deposits will be either profitable or unprofitable. China is certainly taking a huge technological risk. Whatever the outcome, China is demonstrating a new ability to take the lead in a technologically intensive field to secure more resources for its future growth.

2.4 The new normal in Chinese naval presence worldwide

Once China had set itself the strategic goal of becoming a “strong maritime country”, as expressed during the eighteenth party congress, the country’s thinking about its maritime security moved from a regional to a global scale. This adjustment is still ongoing.[72] According to the SOA, “with the expansion of China’s national interest and the stable progress of the construction of the Belt and Road Initiative, problems related to the security of offshore energy resources, strategic sea lanes of communication, overseas nationals and legal entities are increasingly evident. […] Escort missions, civilian evacuation operations, humanitarian assistance and other types of overseas mission are an important mode of protecting national interests and exert international responsibilities. […] A modern system of naval power and a participation in international maritime cooperation have an important meaning to provide strategic support to the protection of our overseas interests”.[73]

This new global outlook on maritime security results from growing “overseas interests” (海外利益 ) and is also encapsulated in China’s defence white paper – to the traditional focus on “offshore defence”, the new concept of “open seas/far seas protection” was added in 2015 and should be confirmed this year when the next white paper is issued. Already, while emphasising the defensive and deterrent role of the “offshore defence strategy” beyond the first island chain (a concept important in China’s strategic defence thinking), China’s 2010 white paper hinted at this new role when it referred to a “new method of logistic supports for sustaining long-time maritime missions” for “missions other than war”.[74] China’s 2015 white paper formalised this transition when it changed the wording to combine “offshore waters/near seas defence” with “open seas/far seas protection”.[75] The white paper called for a modern navy consisting of a “combined, multifunctional, and efficient marine combat force structure” which will allow “strategic deterrence and counterattack, maritime manoeuvres, joint operations at sea, comprehensive defence and comprehensive support”. The Academy of Military Science’s 2013 Science of Military Strategy makes clear that the protection of the sea lanes of communication is important for the navy, and that responding to the strenuous (十分繁重) strategic pressure on China’s maritime trade and fishing activities is becoming a “regular strategic mission” (经常性的战略任务 ) for the navy. It also advocates the construction in “good time” of aircraft carrier battle groups.[76]

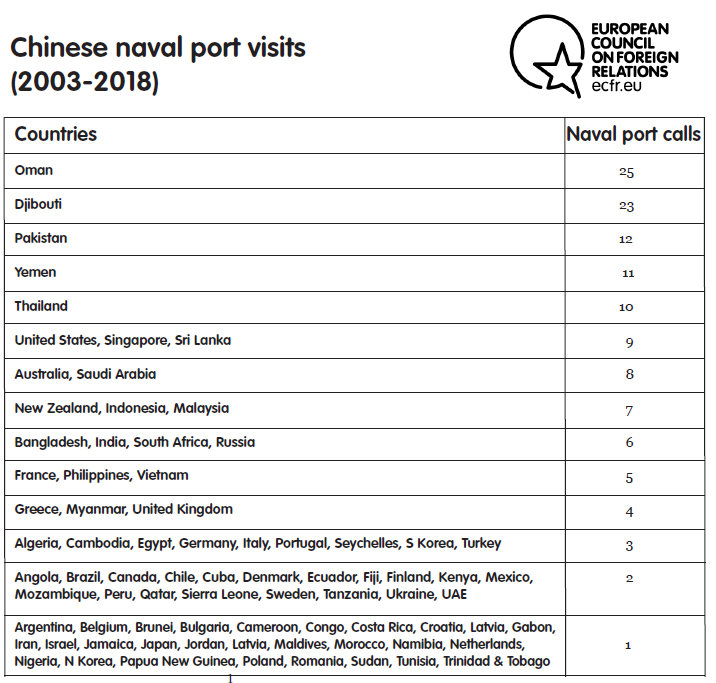

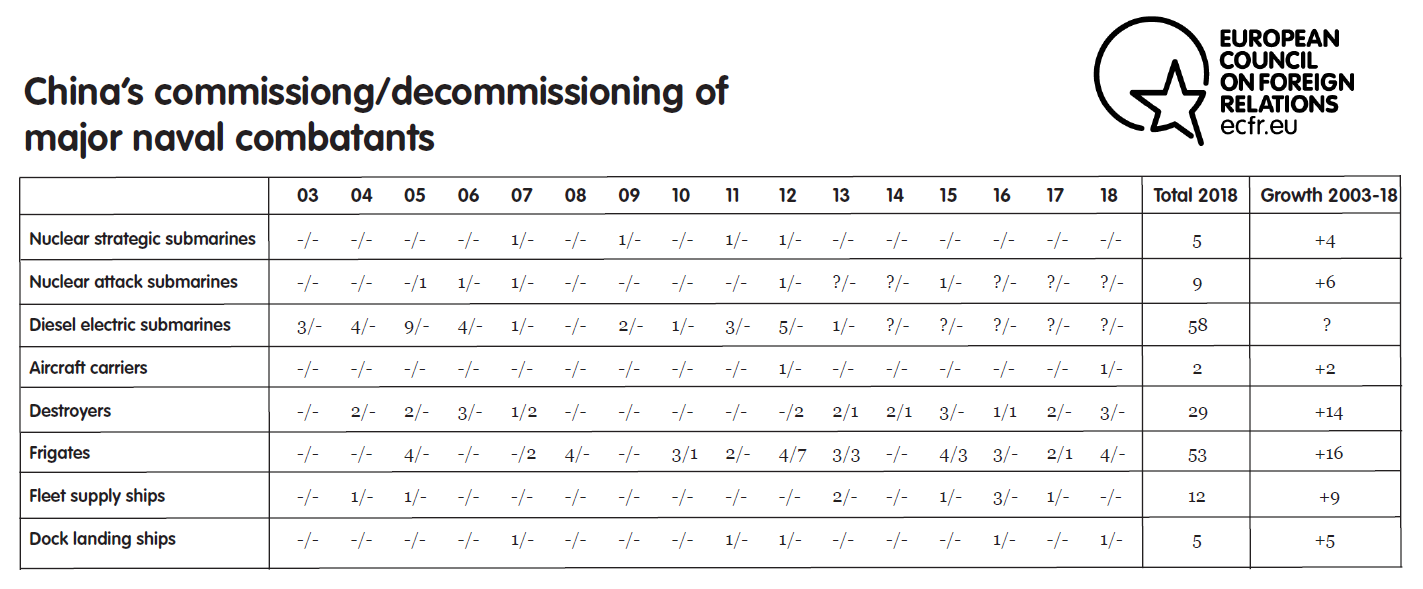

Those objectives are still in line with offshore defence but now envisage new activity taking place in waters further from China itself. Since 2002, China has completed 50 major surface combatants including one carrier, 22 destroyers – including 20 fitted with long-range air defence missiles – and 29 missile frigates – including 27 fitted with the medium- to long-range air defence missiles (see table showing commissioning of surface combatants and submarines in the PLA Navy, 2013-2018). Most of those escorts are equipped with towed arrays that give them an anti-submarine warfare capability previously non-existent in the PLA Navy (PLAN). These new ships have replaced similar numbers of much less capable platforms and have given the People’s Liberation Army Navy (PLAN) an ability to operate in the 500-1,000-nautical mile radius beyond the first island chain in the western Pacific”. Since 2008 they have deployed permanently to the “Far Seas”, the Indian Ocean, for anti-piracy patrols and engage in worldwide naval diplomacy: between 2003 and the end of 2017, PLAN warships have made more than 290 port visits worldwide in all five continents (see table).

In 2017 and for the first time, China demonstrated its ability to conduct multiple deployments worldwide with four task groups active at the same time. Between July and September, the 26th anti-piracy flotilla extended its Indian Ocean tour to European waters, calling at Russia, Finland, Latvia, Belgium, the UK, and France. Meanwhile, the Chinese naval hospital ship, Peace Ark, engaged in its first tour of Africa’s west coast, offering free medical services around the Gulf of Guinea. Beijing also dispatched two surface groups to participate in the Thailand fleet review and to carry out exercises with the Russian Pacific fleet before calling at Vladivostok. This feat was made possible by a spectacular increase in China’s logistic fleet with its number rising from three to 13 fleet support ships so far. Naval visits usually reveal zones of influence, prioritised operational zones, intelligence collection objectives, and cooperation priorities. Overall, China has put the emphasis on showing the flag and displaying friendly diplomacy towards every nation. Since 2008 and its deployment of 27 anti-piracy patrols to the Indian Ocean, it has maintained a balanced relationship between the West and its strategic partner of Russia. Although the relationship with Moscow is privileged and should logically include intelligence-sharing about the US Navy, Beijing has welcomed Washington’s invitation to participate in the unsophisticated phase of the RIMPAC annual exercises.

The Chinese navy deployed in European waters in 2012, 2015, 2016, and 2017. After a first exercise in the Mediterranean with the Russian navy in May 2015, the PLAN conducted anti-submarine warfare and air defence drills with the Baltic fleet off Kaliningrad in July 2017. Referring to the choice of the Baltic Sea – an area of heightened tension between Russia, the US, and NATO – the Chinese journal Global Times observed that “by sending its most advanced guided-missile destroyers, China expressed its ‘sincerity’ to Russia and also sent a strong signal to other countries who plan to provoke us”, namely the US.[77] On this interpretation, the Sino-Russian exercise in the Baltic is a show of solidarity to Moscow, reciprocating Moscow’s show of solidarity to Beijing during the September 2016 Russo-Chinese exercise in the South China Sea. But the same Baltic Chinese task group then toured NATO countries including Latvia and the UK, two of the most vocal critics of Russia, signalling Beijing’s intention to remain neutral. In the words of a Russian naval analyst, the PLAN mission that included joining the Baltic Sea exercises showed “the intention of China to maintain good relations with all European states”.[78] But as a side benefit, it allowed China to respond to the publicised transits of French and British warships in the South China Sea. In other regions, China has followed a similar approach, visiting India, its competitor, as often as its tacit ally Pakistan. It has also called equally at the naval bases of arch-rivals Saudi Arabia, Qatar, Iran, and Israel. But overall, the Xi Jinping years have seen a globalisation of China’s naval presence, a trend that will intensify in the foreseeable future.

The Chinese navy’s current out-of-area deployments resemble those of the Soviet navy in the wake of the 1962 Cuban crisis. Then, the Soviet Union vowed never to seek foreign bases, initially expanding its area of operations using large auxiliary vessels that at first made up for the lack of foreign bases. Soon enough, however, Moscow set aside its initial reservations and allowed the Soviet navy to use foreign ports, namely in Syria (1967), Egypt (1967-73), Algeria (1969, renewed in 1978), Cuba (1970), Guinea Conakry (1971), Somalia (1972-77), Benin (1977), São Tomé and Príncipe (1978), and Vietnam (1979). Albeit limited, those naval facilities helped the Soviet Union increase its overseas deployments. It is not entirely out of the question that China could follow the same path to protect its “overseas interests”.

In December 2015, the PLA confirmed that China and Djibouti had reached an agreement to build an overseas “logistical base” (保障基地) in Djibouti. According to the Ministry of Defence, the base will allow China to carry out “international obligations” through three types of mission: escort as part of the anti-piracy mission, a transit point for peacekeeping, and humanitarian assistance.[79] China is the seventh country to have a facility in the small state, after France, the US, Italy, Germany, Spain, and Japan. The PLAN deputy commander officially put the base into service in August 2017. That said, General Thomas Waldhauser, the head of US Africa Command, expressed his discomfort at the Chinese base’s proximity (10 miles) from Camp Lemonnier, the only permanent US military installation in Africa. Thanks to the debt contracted by Djibouti on other infrastructure projects, the Chinese government is reportedly paying just $20m annually to lease the base, nearly four times less than the US ($70m) – rumours even circulate that China does not pay anything.[80]

It is evident from Chinese statements since 2016 that Djibouti represents a new approach to Chinese presence overseas rather than an exception. During his press conference at the National People’s Congress in March 2018, foreign minister Wang Yi said that China was “trying to build some necessary infrastructure and logistical capacities in regions with a concentration of Chinese interests” [responding] “to actual needs and to the wishes of the countries in question”.[81] The usual line that it is strategic for China to align military modernisation with the pace of economic growth now justifies the importance of “overseas support pivots” (海外驻点 ) to enable power projection and protecting China’s overseas interests, according for example to Admiral Yin Zhuo, a frequent commentator in the Chinese media.[82]

It is thus a matter of the right conditions being met rather than of whether China will proceed to build new “overseas logistical facilities” for its navy. And the PLAN is not alone, as inter-services competition has not disappeared in China. It appears that the People’s Armed Police’s request for a presence in Djibouti was rejected, as the base is operated by the navy only. Under such circumstances, the PLA Air Force may put up a legitimate request for overseas facilities, especially because long-range refuelling remains a major obstacle for its transformation into a global force.

For more than 25 years, speculation has flourished about Gwadar, the Pakistani port situated 130km from the Iranian border and 600 km from the main port of Karachi. So far the project is purely commercial. Commenting on the plans, Dostain Khan Jamaldini, chairman of the Gwadar Port Authority (GPA) since 2013, explains how a small fishing village is being painfully transformed into a “smart” port city with the ultimate goal that it will be self-sufficient, sustainable, and serve the entire region as well as western China through the Kashgar-Gwadar corridor. With the new concept of “far seas protection”, there has been renewed speculation in the Chinese media regarding the potential role of Gwadar as a PLAN naval base. Today, Gwadar harbours a small Pakistani naval base equipped with two Chinese-built 600-ton corvettes working with the 20,000-strong Pakistani Special Security Division team established in Balochistan to protect Chinese workers. Beijing turned down Pakistani proposals to turn Gwadar into a base and in January 2017 Jamaldini made it clear that there is no such plan: “another misperception is that the Gwadar Port is becoming a naval base. Let me, as Gwadar Port chairman, strongly underline that this port is a pure commercial area.”[83] Asked about the future of Gwadar in May 2017, a Chinese scholar close to the PLAN was more circumspect: “everything is changing; in the short term, we won’t be seeking other naval support bases, in Gwadar or elsewhere but who knows what will come later; we may repeat what we did in Djibouti”.[84]

When thinking about the next steps China might take to support naval deployment along the Maritime Silk Road, it is worth drawing the right lessons from Djibouti. If the same modus operandi repeats itself, a key element will be China’s cautious approach, linking the decision to build a base to an on-going Military Operation Other Than War (MOOTW) that can be understood by the international community as a contribution to international security. From that perspective, a base in Gwadar or in the Maldives would mark a huge break in Chinese foreign policy. Building a naval base without any link to such operations would amount to a choice by China to strike an aggressive posture, which is only possible if strategic competition with the US intensifies to levels reminiscent of the Cold War.

For Europe, this global Chinese presence and the emphasis on MOOTW creates cooperation possibilities, albeit limited ones. Chinese researchers acknowledge that the Gulf of Aden’s escort task forces constituted a major step towards the navy’s new role protecting trade routes, stressing the importance of cooperation with other navies to fulfil this mission. Departing from the original intent, the anti-piracy patrols led China to protect anyone joining its convoys and to cooperate with other navies albeit without agree to take part in a task force under another nation’s authority – in other words, as long as they do not have to take orders. Joint escorts of the World Food Programme’s shipments to Somalia were conducted in cooperation with the EU, on an unequal footing – European ships ensuring most of the escorts, with China conducting just one annually.[85] In a scenario of a new Gulf War, China would most likely share the European goal of maintaining freedom of navigation. In such a circumstance, China would again be a partner for evacuations, escorts, and perhaps for mine warfare operations, given the fact that many Iranian mines are of Chinese origin.

Would China use naval forces to influence events ashore in such a way as to be hostile to European interests? In October 2015, with the Liaoning aircraft carrier conducting its sea trials with barely 10 fighter aircraft available, the Lebanese and Israeli press speculated that it was heading for Syria to participate in the air strikes alongside the Russian air force, a rumour that a PLAN spokesman strongly rejected.[86] In fact, China is already able to influence events through MOOTW. Researchers from the Dalian Naval Academy and from the Wuhan Naval University of Engineering have stressed the need to project soft naval power to augment China’s influence in the world. Chinese analysts described the hospital ship Peace Ark’s seven deployments to the Indian Ocean, to the Philippines, to Latin America, and to west Africa – Codenamed “Mission-Harmony” – as “an ideological weapon for shaping a favourable environment for the PLAN”.[87] China still lacks a comprehensive maritime strategy but it wants to give the image of a peace-loving “strong maritime country” that, unlike Western hegemons, is not seeking sea power to interfere in other countries’ internal affairs. The Academy of Military Science makes it clear that MOOTW are important for testing equipment and boosting the navy’s capabilities and that international security cooperation by the navy provides opportunities to reinforce the country’s “power of discourse and influence in international maritime security affairs”.[88] But unlike the Soviet Union in the cold war days, Beijing has so far displayed no intention of confronting other navies on the high seas, outside of the two island chains in the western Pacific where China’s defined core interests – Taiwan and maritime sovereignty issues – are at stake and where Beijing seeks to weaken the US presence, and ultimately gain dominance.

2.5 Responding to intensified strategic competition in the Indo-Pacific

Notwithstanding fundamental differences between the Chinese and Soviet navies’ behaviours, Beijing’s maritime ambitions are not expanding in a global vacuum. Increasingly, they justify the formation of a coalition in the form of quadrilateral cooperation between the US, India, Japan, and Australia to balance China’s rising influence in the Indo-Pacific. The idea is not new but it gained sudden traction in 2017, acquiring its own acronym: the Quad.

The first move has been the adoption of new terminology: the “free and open Indo-Pacific”. According to Rory Medcalf, an early advocate of the Indo-Pacific concept, the Maritime Silk Road is an “Indo-Pacific with Chinese characteristics”, as it unites these two regions in a single geopolitical space and seeks to define their strategic dynamic.[89] The commanders-in-chief of the four navies appeared together at the Raisina Dialogue in Delhi in January 2018.[90] Talks are taking place about the feasibility of an alternative scheme to the BRI to finance infrastructure.[91] India and Japan have already cooperated successfully to prevent China from financing infrastructure in Bangladesh.[92] A consortium led by Sumitomo won the contract for building a port and a coal-fired power plant in the Matarbari district, with the largest loan ever provided by the Japan International Cooperation Agency.[93] Japan’s involvement makes up for India’s lack of financial power to relieve Colombo from the burden of is Chinese debt.

The quadrilateral cooperation has clearly emerged in order to oppose China’s BRI and preserve a “free and open Indo-Pacific”.[94] It aims at a future international order, focused on the maritime domain with radical divergences of interpretation over UNCLOS in the South China Sea which are also shared by European nations. It echoes the Trump administration’s much tougher stance on China. The December 2017 National Security Strategy described China (and Russia) as challenging “American power, influence, and interests” and “attempting to erode American security and prosperity”.[95]

China has responded by calling the Quad a “quadrilateral alliance” (四国联盟), even though the Quad only includes two bilateral alliance treaties, linking the US with both Japan and Australia. In the words of a Chinese Academy of Social Sciences scholar, “Regardless of how much the four countries vow to protect the international liberal order, its norms including freedom of navigation, the essence of their strategy is to balance China”.[96] Notably, the word “containment” (遏制 ) has reappeared in Chinese publications.[97]

While Chinese diplomatic language denounces a “cold war mentality”, there is so far no concrete evidence that China will seek an upfront confrontation with the Quad. In fact, the current modus operandi of avoiding direct confrontation while consolidating Chinese strategic positions wherever possible – in Djibouti, in the Indian Ocean and in the South China Sea – might be sustainable in the short to medium term.

The Maldives is emerging as a test case for China-India relations and the credibility of “free and open” Indo-Pacific quadrilateral cooperation.[98] As in Sri Lanka, the size of the Maldives’ debt to China is extremely divisive politically. In February 2018, this led to a major domestic crisis, with the pro-China president, Adbullah Yameen, ordering the arrest of members of the opposition parliamentary group and of the Supreme Court after the leader-in-exile of the opposition attacked him over his dealings with China. The Maldives’ political crisis led nationalistic media outlets in Beijing suggest that the deployment of Chinese warships in the Indian Ocean had prevented New Delhi from intervening. From an Indian perspective, the question is whether India should deal with the issue of Chinese influence in its backyard now – “when it has the means to enforce its will on the Maldives” – or continue with non-interference.[99] The rumours that a PLAN task force was in the vicinity of the Maldives at the peak of the crisis in order to deter India from intervening militarily, as it did in 1988, proved untrue. The Chinese flotilla was in the Indian Ocean for a scheduled exercise. But the episode will certainly lead both China and India to step up their game in the archipelagic state.

Another issue is the future of the Russian-Chinese strategic partnership. Although Chinese experts deny the possibility of an alliance with Russia, owing to a range of factors, including a lack of strategic trust, Russia’s ongoing confrontation with the West has led Moscow to a spectacular rapprochement with Beijing.[100] Their common assessment that the West’s promotion of democracy in the Middle East, especially through the military intervention in Libya in 2011, has been a major cause of chaos in the Muslim world, is a key determinant of the current dynamic in Sino-Russian relations. The two countries frame this in terms of defending “strategic stability” – Russian analysts depict it as a response to US ballistic missile defence and the West ignoring Russian concerns over NATO’s expansion to former Soviet states.[101] Some Russian analysts even suggest that Moscow and Beijing may contemplate a joint naval task force in order to deter future Western initiatives. If the Quad takes the form of an anti-China NATO extension, Russia and China might be tempted to form an anti-NATO alliance. Such a development would be tempered by Russia’s good relations with India and Vietnam, two frontline Chinese antagonists. But as cooperation around the Quad idea progresses, the four countries may realise that they should not neglect the Russia factor.

Undoubtedly, this wider strategic context will impose itself upon Europe. A bipolar structure has not yet fully emerged in the Indo-Pacific region. In Brussels, engagement with China remains the dominant approach. The priority today, under a new wave of European realism, is to rebalance the trade and investment relationship with China.[102] Any question of ‘joining’ the Quad is not urgent, and has most relevance for large EU member states with long-range naval capabilities – France and the UK, already active proponents of freedom of navigation. These two countries signal their position to China’s side by sailing through the South China Sea, even though they avoid challenging China directly in the 12 nautical miles zone inside the artificial features in the Spratly Islands. In Europe, the debate on taking sides is only just starting.

3. Conclusion and policy recommendations

China’s policies on facilitating the growth of its blue economy and its construction of a powerful navy are transforming the global maritime environment in which Europeans operate. Both sides seek prosperity and security, and this can create opportunities. But overall the Maritime Silk Road presents Europe with serious challenges, and it will heighten the competition element in Europe-China relations. Europe should not turn its back on the opportunities that exist but it should not turn a blind eye to the challenges either.

- The EU should put in place an EU-wide investment-screening system, and soon. Chinese investment in European ports can be unproblematic – until a critical size is reached. This point is reached when the scale of one project in a single country leads to excessive political influence, although this can also come about through the gradual establishment of a position of dominance which threatens fair competition. In third countries, the growth of Chinese influence through port infrastructure leaves no space for a ‘win-win’ game between Europe and China. In an ideal scenario, a greater Chinese economic presence in unstable states could lead to EU-China crisis management cooperation. But the absence of any significant achievements in this area so far indicates that such an outcome is unlikely. As a result, the EU and its member states should draw a clear line for themselves between investment that helps meet European long-term interests and investment that negatively affects Europe’s competitiveness. Besides introducing an EU-wide screening policy, equally important is the need for reflection within the EU institutions and among member states about how investment-screening should apply to the maritime domain and the blue economy. For internal use, the EU could produce a “white list” of areas where cooperation with China can operate on a basis of reciprocity. The EU should make clear to China that reciprocity should be the basis for investment exchanges in the blue economy. Experts understand that reciprocity is about fairness and non-discrimination, but there is a risk of misinterpretation on the Chinese side. Europeans should seek to mitigate this through clear explanations.

- Europe should look and learn from China’s blue economy as an engine of growth and wealth. Europe should emulate China’s strong and well-funded policies on developing shipbuilding, deep sea exploration, offshore oil and gas exploration and exploitation, shipping, and on the availability of Chinese corporations and policy banks in supporting infrastructure projects worldwide. The EU and EU member states should encourage innovation in order to preserve a European niche of expertise in key sectors of the blue economy. That said, Europeans should keep in mind that a key Chinese weakness is the risk of public resources being wasted because of non-performing loans.