Europe’s alternatives to Russian gas

Europe’s new Energy Union aims at securing European energy supply – but, if not from Russia, where will Europe obtain its gas?

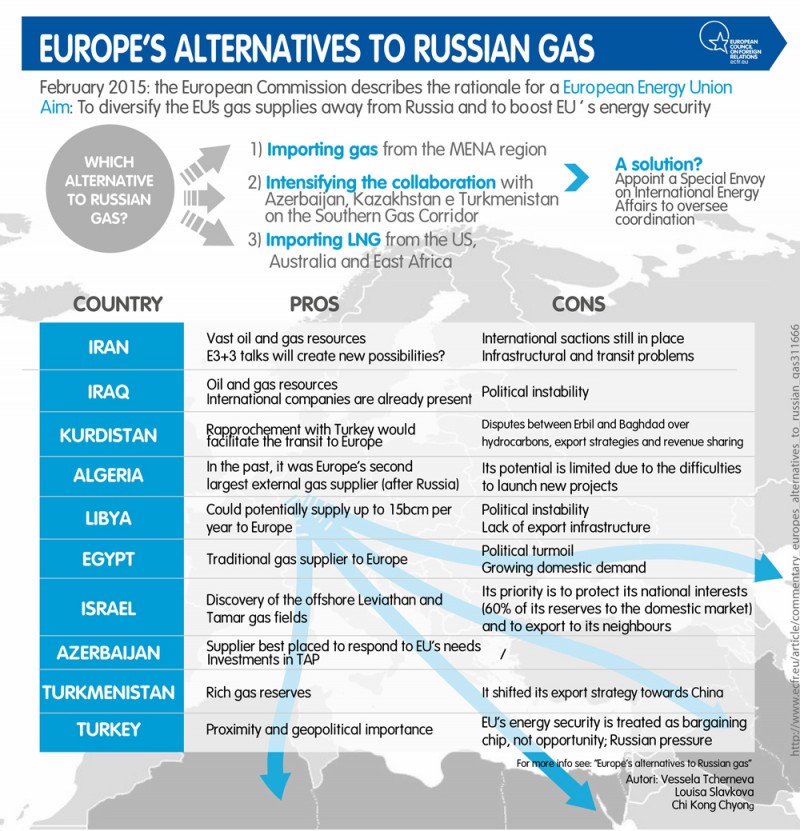

In February, the European Commission published a Communication that describes the rationale for a European Energy Union, which was first proposed by then Polish Prime Minster Donald Tusk, now president of the European Council.

Energy insecurity in the European Union has two main sources: gaps in the integration of the European energy market, especially in regions such as Central and Eastern Europe, and disruptions of imports. To combat these problems, the Energy Union strategy focuses in two of its five dimensions on removing energy islands and bottlenecks from the infrastructure map of Europe, and on developing solidarity mechanisms for preventive planning and emergency responses for scenarios in which supply is disrupted.

Part of the aim of the Energy Union is to diversify the EU’s gas supplies away from Russia, which has already proved to be an unreliable partner.

Part of the aim of the Energy Union is to diversify the EU’s gas supplies away from Russia, which has already proved to be an unreliable partner, first in 2006 and then in 2009, and which threatened to become one again at the outbreak of the conflict in Ukraine in 2013-2014. With its February 2014 Communication, the Commission acknowledged the foreign policy implications of energy policy and the need for a coordinated energy policy, something that was largely under-emphasised in previous discussions about the future of EU energy security.

The Energy Union strategy suggests a number of measures to boost Europe’s energy security, both internally and externally. One of the external aspects involves granting the Commission a watchdog role in the process of the renegotiation of Intergovernmental Agreements (IGAs) with third countries to ensure compliance with European rules and security of supply criteria. This would enable the Commission to raise concerns about projects such as South Stream whenever they fail to accommodate European interests. The other aspect provides an answer to the problem of dependency on Russian gas.

Although diversifying away from Russian gas is not unrealistic in the medium term, several technical and political obstacles must be overcome.

Russia is the main supplier of crude oil and natural gas to the EU, and although diversifying away from Russian gas is not unrealistic in the medium term, several technical and political obstacles must be overcome. In the short term, part of the solution lies in targeted investment and in mobilising existing EU instruments to improve internal connections and expand links with EU neighbours. The February Communication mentions strengthening four alternative routes and sources of gas supplies, as well as creating regional hubs to deal with potential disruptions. Among the alternatives are:

· Importing gas from the Middle East and North Africa;

· Intensifying work on the Southern Gas Corridor through Azerbaijan, Kazakhstan, and Turkmenistan;

· Importing Liquefied Natural Gas (LNG) from the United States and Australia as well as from East Africa.

Our analysis covers the timeframe until 2025. Most of the EU’s Russian gas contracts are expected to expire within this period, which will provide member states with the option to diversify their sources of supply. Ensuring European energy security will require more than investment in infrastructure and energy-specific know-how about interconnections and gas transit disruptions. It should form part of European energy diplomacy, with more concerted planning and action on the external side, including dialogue with global actors such as China (which is expected to be the major energy demand centre), the US, and Turkey (which is still only an observer in the Energy Community). This requires better coordination and shared decision-making within the Energy Union, with input both from the Commission and from the European External Action Service. A Special Envoy on International Energy Affairs could be appointed to oversee better coordination.

Energy should be central to the EU’s policy towards its neighbours, and the EU should also take a leadership role in promoting energy security beyond its borders.

Europe’s external energy security is linked to its neighbours, and its relations with these neighbours is managed by the European Neighbourhood Policy. Energy should be central to the EU’s policy towards its neighbours, and the EU should also take a leadership role in promoting energy security beyond its borders.

Regional alternatives

Iran, Iraq, and Kurdistan

With their vast oil and gas resources, Iran and Iraq constitute potential sources of energy supplies for Europe. Iran does not seem to represent a viable alternative to Russian gas, at least in the short to medium term. However, if the ongoing E3+3 talks over Iran’s nuclear programme reach a successful outcome beyond the tentative deal reached in Lausanne, it would create possibilities to explore the country’s resources and integrate it into the regional energy infrastructure.

Substantial investment would be needed to bring gas to the northwest to tap into Europe’s Southern Gas Corridor.

The political constraints to using Iranian energy, such as the international sanctions now in place, are obvious. But there are also infrastructural constraints, such as the geographical distribution of resources in Iran relative to its consumption, as well as the lack of production and export infrastructure. Iran’s gas resources (for example, the South Pars field) are in the south. Therefore, substantial investment would be needed to bring gas to the northwest to tap into Europe’s Southern Gas Corridor.

Iraq – and in particular, Kurdistan – is another potential supply option for Europe: it has massive oil and gas resources and international exploration and production companies are present and active. However, the parlous political situation in the country presents a major impediment to large-scale investment in developing the production and export capacities that would be needed to bring its energy to Europe.

The rapprochement in recent years between Turkey and the Kurdistan Regional Government in Iraq (KRG) has opened up the option of exporting gas supplies from Northern Iraq.

The rapprochement in recent years between Turkey and the Kurdistan Regional Government in Iraq (KRG) has opened up the option of exporting gas supplies from Northern Iraq. The KRG could play a large part in supplying Turkey with natural gas. And, given its huge gas reserves, it could also become a supplier to Europe in the long run, if disputes between Erbil and Baghdad over hydrocarbon development, export strategy, and revenue sharing are sorted out.

Algeria

Algeria has in the past been Europe’s second largest external gas supplier (behind Russia), supplying around 25 billion cubic metres (bcm) via pipelines and 13.5 bcm via LNG for a market share of 9 percent in 2013. Algeria’s export potential is limited going forward, however, since it is struggling to launch new projects and those that are scheduled to come on line in 2015-2017 are not enough to compensate for the decline of its mature production fields. In addition to the supply side constraints, the domestic market is expected to grow, particularly in the utility, desalination, and industrial and chemical sectors. These two factors limit the extent to which Europe will be able to rely on additional supplies from Algeria in the coming years to replace the decline in European production.

Libya

Algeria’s neighbour, Libya, could theoretically supply up to 15 bcm per year to Europe by the mid-2020s. In 2013 Libya produced 12 bcm and supplied around 5 bcm to Italy via the Greenstream pipeline. Unlike Algeria, Libya is expected to remain a net exporter, since the growth of its domestic market remains slow due to continued economic and political unrest in the country. However, its net export position is limited by the lack of potential for growth in Libya’s supplies, which is constrained by lack of export infrastructure. At the moment, Libya exports gas to Europe via the Greenstream pipeline (11 bcm per annum), which connects the country with Sicily.

Libya is expected to remain a net exporter, since the growth of its domestic market remains slow due to continued economic and political unrest in the country.

Libya also has an LNG export facility (in fact, the second LNG export plant ever built, after Algeria’s), which has a nameplate capacity of 3.2 million tonnes per annum. However, the facility is not in operation because of the heavy damage it has sustained during the conflict. It is unlikely to come back online in the short to medium term.

Thus, Libya’s gas export growth would have to be supplemented by new pipelines and/or by LNG plants, which, given the political uncertainties, seem unlikely to materialise any time soon.

Egypt

It is highly unlikely that Egypt will remove energy subsidies in order to moderate the growth of demand.

Egypt is another traditional gas supplier to Europe, but it too is becoming an importer because of its growing domestic market – over the last 20 years, consumption has grown by 8 percent a year. Domestic demand is expected to catch up with production by 2015, limiting the country’s export potential. It is highly unlikely that Egypt will remove energy subsidies in order to moderate the growth of demand: the political turmoil in which the country has found itself since 2011 makes the Egyptian government reluctant to adopt unpopular measures such as increasing utility and gas prices. Therefore, Egypt is likely to become a net importer.

Israel

The discovery of the offshore Leviathan and Tamar gas fields in the Eastern Mediterranean Sea could make Israel a regional gas exporter. These two fields have total estimated reserves of 792 bcm. Despite its potential for exports, however, Israel’s priority has been to protect its national interests, including its energy security: 60 percent of its gas reserves must be supplied to the domestic market.

Israel has seemed to be more willing to supply its gas surplus at market prices to neighbouring countries (notably, Egypt and Jordan) rather than to invest in expensive infrastructure to tap into European markets.

Moreover, given the expected growth in regional energy demand, Israel has seemed to be more willing to supply its gas surplus at market prices to neighbouring countries (notably, Egypt and Jordan) rather than to invest in expensive infrastructure to tap into European markets. Israel has agreed to supply 45 bcm to Jordan and negotiations are under way to supply excess gas through a pipeline to Egypt’s LNG facilities, which represents a potential export route for Israeli gas. Another export option would be to supply gas to Turkey – but in view of the political disagreements between the two countries, that does not seem likely in the near term.

Azerbaijan

Azerbaijan is the supplier best placed to respond to the EU’s strategy of diversifying gas supply away from Russia. Azerbaijan has long been cooperating with Western energy companies on projects such as the Azeri-Chirag-Deepwater Guneshli oil project and the Shah Deniz gas condensate project (both led by BP), as well as the Baku-Tbilisi-Ceyhan (BTC) and the Baku-Tbilisi-Erzurum (BTE) pipelines. Thus, the scope for increasing gas supply from Azerbaijan seems to be simply a matter of the economics of the potential supply projects.

Azerbaijan is the supplier best placed to respond to the EU’s strategy of diversifying gas supply away from Russia.

The supply is expected to come from the second phase of the Shah Deniz project, with an estimated cost of over $45 billion, or $380-430/billion cubic metres at the Turkey-Greece border, and from the Umid gas field (SOCAR and Nobel Oil). The two projects could potentially supply up to 18-19 bcm per year of gas by 2020, with at least 6 bcm committed to the Turkish market and 10 bcm to Greece, Albania, and Italy. In 2014, the Shah Deniz consortium finally agreed to commit gas resources to the Trans Adriatic Pipeline (TAP), which will bring Azeri gas to Europe through Turkey; although it has a small transport capacity, this project will certainly contribute to the EU’s diversification efforts.

Turkmenistan

Turkmenistan’s rich gas reserves are a logical source for European supplies and the option of obtaining gas from the country has been discussed for a long time. However, after long and unsuccessful negotiations on building the Trans-Caspian Pipeline under the Caspian Sea to bring Turkmen gas to Europe, Turkmenistan has shifted its export strategy towards China. China has secured most of the prospective and relatively cheap upstream projects: the first two phases of the Yolotan gas field (up to 60 bcm/year) and the Bagtyyarlyk gas fields (15-30 bcm/year). And in 2003, Moscow managed to make Ashgabat commit its entire gas export capacity to Gazprom for the next 25 years.

After long and unsuccessful negotiations on building the Trans-Caspian Pipeline under the Caspian Sea to bring Turkmen gas to Europe, Turkmenistan has shifted its export strategy towards China.

Competition with China and Russia is one factor militating against Turkmen gas being sent to Europe. Another is the need to resolve the Caspian Sea water boundaries among its five littoral states, which is required in order to allow the construction of the Trans-Caspian Pipeline. That said, negotiations on the issue between Turkmenistan and Azerbaijan, which had been stalled, have been revived as a result of the current crisis in Ukraine.

Turkey

Turkey has been able to implement a fairly successful energy policy, securing significant volumes of hydrocarbons and attracting huge investments for the country’s ambitious energy transportation projects. The recent discussion of the possibility of building a “Turkish Stream” in place of the failed South Stream project was yet another illustration of the key transit position of Turkey with regard to Europe. In a sense, the key to Europe’s diversification lies with Turkey – but the relationship between the EU and Turkey has been somewhat icy for the past few years.

In Ankara, Europe’s energy security is treated more as a bargaining chip than as a shared strategic vision.

Arguably, contributing to European energy security is no longer an objective in itself for Turkey. In Ankara, Europe’s energy security is treated more as a bargaining chip than as a shared strategic vision. That being said, especially when it comes to Russian pressure on Azerbaijan, the EU and Turkey’s interests are fully aligned on routing more Azerbaijani gas through Turkey to Europe, as opposed to allowing Moscow to have more of it channelled to Russia.

Recent major gas discoveries in the Eastern Mediterranean (offshore of Israel and Cyprus) may be used to supply the Turkish market and transported beyond to Europe, if the underlying geopolitical frictions can be sorted out. EU diplomatic engagement could be critical here: persuading the Republic of Cyprus to allow an Israeli pipeline to pass through its Exclusive Economic Zone (EEZ) would give the EU an instrument to influence Turkey’s position on other issues.

The EU could lead a diplomatic initiative in which, together with Turkey and the US, it could mediate between the governments of Erbil and Baghdad.

As mentioned above, closer relations between Turkey and the Kurdistan Regional Government in Iraq (KRG) and Turkey in recent years have made possible the option of gas supplies from Northern Iraq. The KRG could supply Turkey with natural gas, and in the long term could also supply Europe, if Erbil and Baghdad could resolve their disputes over development, export strategy, and revenue sharing. Turkey has little diplomatic leverage to enable it to contribute to settling the dispute. So, the EU could lead a diplomatic initiative in which, together with Turkey and the US, it could mediate between the governments of Erbil and Baghdad.

If the nuclear issue is resolved, Iran could well become an exporter of gas to Europe via Turkey towards the second half of the decade, though that would also require fundamental reform in the Iranian hydrocarbon sector.

Turkey’s role as a transit corridor for Azerbaijani gas should also be mentioned, but Europe’s leverage here has been considerably reduced since the pipeline to be used is the Trans-Anatolian Natural Gas Pipeline (TANAP, owned by Azerbaijan and Turkey) as opposed to Nabucco (which was a European consortium) – and particularly because of the way this happened, with Nabucco stalled for several years and causing resentment.

Turkey will need vast investment in its energy infrastructure, and also liberalisation and reform of its electricity and gas markets.

In the longer term, Turkey will need vast investment in its energy infrastructure, and also liberalisation and reform of its electricity and gas markets. Solid EU-Turkey energy cooperation could deliver these goals, as the EU has already played an important role in this area. A competitive energy market could well lower the country’s energy bill, while reinforcing an energy infrastructure that would help Europe’s energy diversification.

The new developments around TAP and the cancellation of South Stream highlighted yet again the importance of the Southern Gas Corridor. Turkey’s role is crucial for the energy diversification of Europe, and of its southeast and south in particular. The perception of Turkey as a gas hub is very high on President Recep Tayyip Erdogan’s agenda, and the EU would be well served by enhancing its political dialogue with Turkey on the issue of gas transit.

Europe’s goal of significantly diversifying away from Russian gas is challenging but not impossible in the short to medium term.

To sum up, Europe’s goal of significantly diversifying away from Russian gas is challenging but not impossible in the short to medium term (through 2020-2025). Among the many challenges are the uncertainties regarding some of the most promising non-Russian gas supply options, such those from the Middle East and Caspian regions. The resolution of these uncertainties depends on the actions and political will of others (such as the US, Russia, and China) as well as Europe’s ability to speak in its own voice. This latter would be significantly boosted by the introduction of a Special Envoy.

The European Council on Foreign Relations does not take collective positions. ECFR publications only represent the views of their individual authors.